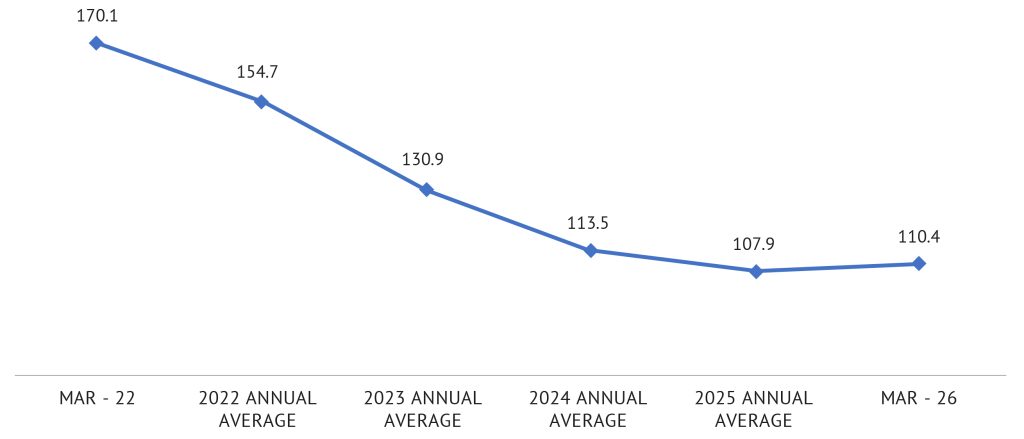

The Nigerian poultry industry finds itself at a contradictory crossroads. On the global stage, agricultural input markets have undergone a measured normalisation, with international grain benchmarks softening from their post-pandemic and conflict-driven peaks in 2022, allowing global producers a degree of margin recovery. Yet this relief has not translated into lower domestic poultry costs, where eggs sold for as much as ₦8,500 per crate in late March and day-old chick prices climbed sharply, reflecting a crisis rooted less in world markets than in Nigeria’s own production structure.

Figure 1: FAO Cereal Price Index (2022–2026)

Source: Food and Agriculture Organization (FAO)

The immediate problem is a supply-side breakdown. Poultry producers are facing a shortage of day-old chicks (DOCs), higher hatchery costs, weak feed supply transmission, and persistent exposure to foreign exchange volatility. In practical terms, this means that even when international maize and soymeal prices soften, local producers do not receive full relief because logistics costs, energy tariffs, insecurity, and imported veterinary inputs keep landed production costs high. The result is a poultry system that is becoming less responsive to improved global conditions and more vulnerable to domestic bottlenecks. As we navigate the second quarter of 2026, the diagnostic is grim: the industry is facing a perfect storm where skyrocketing unit costs and constrained production (estimated at around 650,000 metric tonnes in 2026 – around 30% of national demand) meet a population where nearly 35 million people are at risk of acute food insecurity.

The Chick Shortage

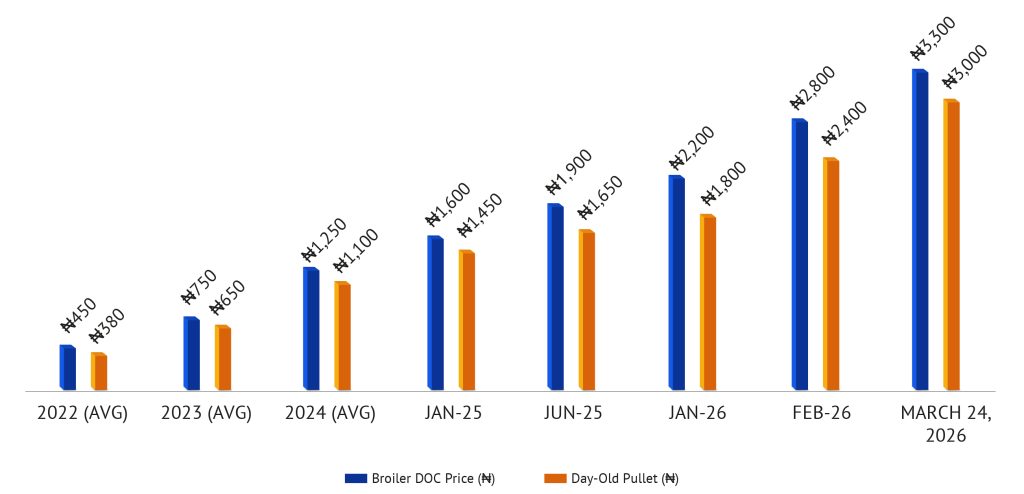

In early 2026, the price of a day-old pullet surged from roughly ₦1,800 in January to over ₦3,000 as at 24 March 2026, with some broiler DOCs peaking at ₦3,300. We believe that this is clearly a clinical symptom of an exhausted model. Because Nigeria remains tethered to international genetics for high-performance stock, every downward tick of the Naira is instantly reflected in the hatchery gate price.

That dependence has left the industry with little buffer against currency weakness. Once the naira weakens, the cost of imported genetics and inputs is quickly transmitted into local hatchery prices, and small producers are typically the first to be squeezed out. The most exposed operators are mid-scale and smallholder farmers, who lack the balance sheet strength to absorb repeated input shocks.

For decades, feed has accounted for 70% of production costs, but in the current 2026 environment, that figure has swelled to nearly 80% on intensive commercial farms. Even where local maize and soy availability improves, prices remain elevated because of transport frictions, insecurity in key producing areas, post-harvest losses, and weak storage infrastructure. This means the sector is not just dealing with expensive grain; it is dealing with a broken conversion chain from farm to feed mill to hatchery to retail market. In that environment, the headline grain price matters less than the actual landed cost faced by producers. The poultry value chain is therefore operating under persistent margin compression, with many farmers reducing bird numbers or exiting altogether.

Figure 2: Nigeria: Day-Old Chick & Pullet Price History (2022–2026)

Source: National Bureau of Statistics (NBS) – Selected Food Price Watch, BusinessDay Agriculture

The China-Nigeria Partnership

In a characteristic move towards big-ticket solutions, the Federal Government has placed a massive ₦900 million bet on industrialisation through an integrated poultry partnership with Chinese private equity. This initiative envisions the establishment of six massive industrial clusters, with pilots already breaking ground in Oyo and Kaduna, each capable of producing up to one million eggs daily, and is designed to achieve food security through sheer scale and “Backward Integration.” Each of the six planned mega-farms is designed to be a self-sustaining ecosystem, dedicating 10,000 hectares of land per farm for the cultivation of maize and soybeans. In principle, the model could improve production efficiency by combining hatcheries, feed processing, abattoirs, and power generation within one integrated system.

The main policy question is not whether the projects can produce eggs, but whether they can do so without deepening market concentration. If the farms are run as closed systems with weak local linkages, they could crowd out smaller producers rather than stabilise the wider sector. Their credibility will therefore depend on whether an outgrower framework, feed-stabilisation role, or supply-contract structure is built into the model from the outset. However, from a geopolitical standpoint, however, the partnership still warrants scrutiny. With an estimated 85% of funding for later phases expected from Chinese private equity, analysts need to carefully evaluate long‑term exposure to single‑country financing and infrastructure, including implications for governance, bargaining power, and strategic autonomy?

The MoorBeta Mandate

A more durable solution lies in domestic poultry genetics. Nigeria’s approval of MoorBeta, a local meat-type chicken, developed over a decade by the Institute of Agricultural Research and Training (IAR&T) at Moor Plantation in Ibadan, is an important step towards reducing reliance on imported stock. The bird was reported to reach about 2.8kg in 10 weeks with survival rates above 95% in trials, suggesting that local breeding can deliver commercially viable performance under Nigerian conditions.

That matters because the current production model is biologically expensive. Exotic breeds can perform well, but they require stronger cooling, more intensive feeding, and more stable veterinary support than many Nigerian farms can reliably provide. MoorBeta offers a lower-risk alternative for local conditions, but only if it is scaled beyond pilot release into a national multiplication system with breeder centres, extension support, and commercial adoption incentives.

Technology as Enabler

Technology is best understood as a force multiplier rather than a substitute for reform. AI-enabled feeding systems, remote monitoring, and IoT-based health tracking, particularly in hubs like Oyo State, can improve feed efficiency, reduce mortality, and strengthen farm management, particularly for larger operators with access to capital. In poultry, even small waste reductions can materially affect profitability, so digital tools can make a real difference. However, the risk is that these gains remain concentrated among larger firms. Most smallholders cannot afford the hardware, software, maintenance, and training requirements needed for precision poultry systems. Unless technology deployment is paired with blended finance, performance-based grants, or cluster-based service models, it may widen the gap between a modern commercial core and a struggling informal periphery.

Policy Priorities

Nigeria’s poultry industry does not need a single silver bullet. It needs a compact that aligns industrial scale, domestic genetics, and inclusive productivity support. First, the China-backed industrial farms should be linked to local suppliers through outgrower arrangements, feed procurement channels, and transparent pricing rules. Second, MoorBeta should be moved from scientific achievement to commercial scale through breeder multiplication and farmer distribution networks. Third, technology adoption should be prioritised for organised clusters and mid-tier producers through shared infrastructure and targeted financing.

The larger lesson is that food security will not come from import substitution alone. It will come from building a poultry system that can survive FX volatility, climate stress, insecurity, and capital scarcity without shutting out local enterprise. The ₦8,500 egg crate is therefore not just a price shock; it is a policy warning that Nigeria’s poultry model must become more resilient, more local, and more coordinated.