As of mid-March 2026, the global geopolitical theatre has shifted from a state of uneasy tension to one of active, escalating volatility. The coordinated strikes in early March against Iran by the US-Israel axis have unsettled regional stability and fundamentally dismantled the post-pandemic strategic consensus. For the global analyst community, the primary takeaway is that the “era of cheap energy security” has been effectively terminated. For Nigeria, a nation eternally caught between the windfall of high crude prices and the pitfall of domestic inflationary shocks, the stakes have never been higher.

A Shifting Strategic Paradigm: The Global Landscape

While regional skirmishes have been a perennial feature of Middle Eastern politics, the current escalation represents a radical pivot in US foreign policy – from containment to active deterrence. The US appears to have shifted its strategy beyond a proxy war toward a direct and high-stakes challenge to the regional status quo, aiming, at least on paper, to dismantle Tehran’s ballistic and nuclear capabilities before they achieve irreversible threshold status. As maritime insurance premiums for the Persian Gulf surge – to as much as 3% from c.0.25% of vessel value, the “war-risk premium” has migrated from a derivative market hedge to a daily operational reality for the real economy.

Global supply chains, already fragmented by the “near-shoring” trends of the early 2020s, are being rerouted at immense cost. The Persian Gulf, once the world’s most critical global trade arteries, is rapidly transforming into a contested military zone. For Nigeria, this global instability creates a “forced opportunity” that is as dangerous as it is lucrative. The question remains: can the Nigerian state capitalise on the disruption, or will institutional inefficiencies turn a potential windfall into another exercise in futility?

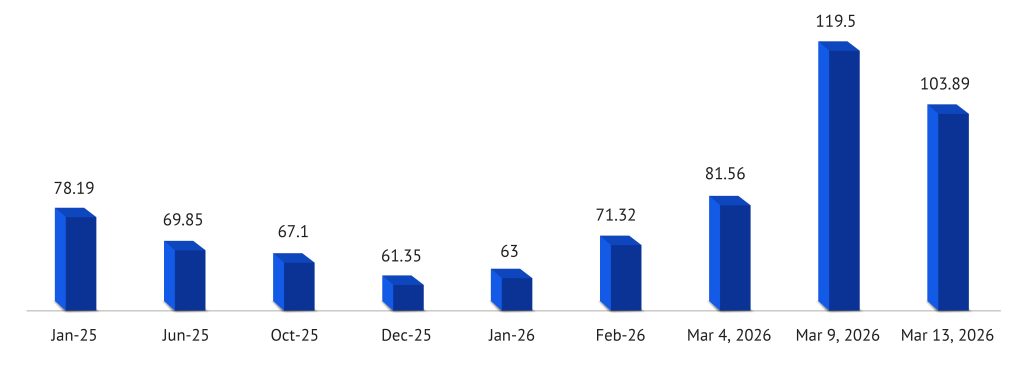

Figure 1: Brent Crude Oil Prices ($’ per barrel)

Source: EIA, Bloomberg, OPEC

The $150 Question: Energy and Commodity Markets

Global energy markets have responded to the March strikes with violent price elasticity. Brent Crude, which maintained a relatively stable range near $80 in February, has transitioned from a steady climb to a vertical spike following the strikes on Iranian military assets near Kharg Island (on 14 March 2026). As at 16 March 2026, Brent had breached the $100 barrier, trading at $105.89 per barrel.

- The Status Quo Scenario: With the Strait of Hormuz effectively restricted and global insurers suspending “War Risk” coverage, we anticipate a near-term expected price range for Brent crude of between $100 and $115. While this provides a fiscal cushion, the primary risk is “volatility fatigue,” where businesses struggle to plan capital expenditure amidst fluctuating input costs.

- The Escalation Scenario: A sustained closure of the Strait of Hormuz, through which roughly 21 million barrels per day (mbpd) of global supply flows, or roughly 20% of global consumption, or direct damage to regional export terminals, makes a breach of the $150 barrier a distinct possibility. However, for a heavily import-dependent economy like Nigeria, the crisis transcends energy volatility. A blockade would catastrophically disrupt the flow of non-oil essentials, including industrial machinery, chemicals, and consumer goods often sourced from Asian markets. As maritime insurance premiums surge and vessels are forced into costly rerouting around the Cape of Good Hope, the landed cost of all imported inputs will rise sharply. This “supply-chain shock” would trigger pervasive cost-push inflation, stifling domestic manufacturing and further eroding the purchasing power of the Nigerian consumer, effectively turning a regional energy crisis into a systemic national economic emergency.

The Emerging Market Trap: Risk-Off and Capital Flight

For emerging markets (EMs), the geopolitical cauldron has abruptly terminated the “easing window” of early 2026. Throughout late 2025, many EM central banks – including the CBN – successfully began lowering interest rates as exchange rates stabilised against a softening US Dollar and inflation trended downwards. However, the escalation of tensions in the Middle East has triggered a classic “flight to safety,” with the US Dollar surging to a yearly high above 100.50 as of 16 March 2026.

This sudden “Risk-Off” sentiment is particularly punishing for frontier markets like Nigeria, where the recent 50-basis-point cut to 26.5% MPR now looks vulnerable. EMs are once again caught in a “Capital Flight Trap.” The progress made in the first quarter of 2026 is being reversed as central banks are forced back into a defensive, hawkish posture to protect their currencies from rapid depreciation, even as domestic growth requires continued stimulus. This creates a stagflationary cycle that could stall the post-pandemic recovery for the foreseeable future. The US Dollar, bolstered by its safe-haven status, continues to strengthen against EM baskets, making “imported inflation” the primary threat to domestic price stability.

The Nigeria Paradox: Volume Over Value?

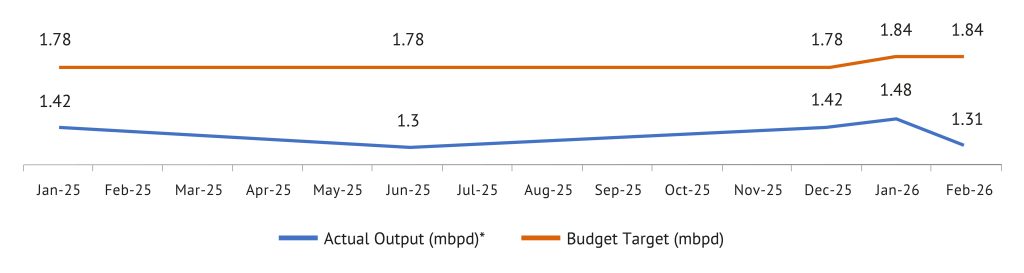

Nigeria’s macroeconomic outlook for 2026 is defined by a deep structural inconsistency. While the current spike in global oil prices provides a degree of fiscal compensation for domestic production shortfalls, the net benefits are significantly moderated by a volume deficit.

Figure 2: Nigeria’s Crude Oil Output: Actual vs. Budgeted

Source: OPEC Monthly Oil Market Report, NUPRC

February 2026 data indicates that output dipped to 1.31 mbpd, from an average of 1.48 mbpd in January, failing to meet both the 1.5 mbpd OPEC+ quota and the ambitious 1.84 mbpd budget target.

From a fiscal standpoint, the $105.89 spot price effectively “protects” the budget’s revenue assumptions (which were based on $64.85 per day). However, the real tragedy lies in the opportunity cost. By failing to meet production targets during a global supply gap, Nigeria is unable to fully capitalise on this historic windfall. This volume shortfall directly reduces the fiscal space available for the government to provide critical social safety nets or energy credits to citizens as domestic petrol prices surge above ₦1,300 per litre. In essence, the price spike sustains the state, but the production failure abandons the citizen.

Adjustment Friction: Navigating Nigeria’s New Market-Reflective Reality

Perhaps the most significant structural shift in Nigeria’s 2026 outlook is the nation’s newfound “nakedness” to global shocks. By dismantling the opaque subsidy regimes and unifying the foreign exchange windows in the preceding years, the Nigerian state has essentially removed its primary macroeconomic shock absorbers. While these reforms were necessary for fiscal health, they have created an environment where a drone strike in the Middle East translates into a price hike at a petrol station in Abuja within hours, rather than months.

This “market-reflective” reality puts Nigeria in a unique position compared to West African peers, who have long been accustomed to higher pump prices. For Nigeria, 2026 is the year of “Adjustment Friction,” where the psychological resilience of the consumer is being tested against a backdrop of raw, unfiltered global commodity volatility.

Reframing the Intervention: From Consumption to Production

As petrol prices at the pump hit ₦1,300 per litre as at 18 March 2026, the debate over a return to fuel subsidies has reached a fever pitch. A more surgical policy alternative is required: supply-side intervention. Rather than returning to the “old wine” of fixing pump prices – a move that would bleed the treasury and invite corruption – policymakers must explore market-based tools to lower the cost of energy production.

The domestic energy equation is now dominated by the Dangote Refinery. With global crude costs surging, the refinery’s gantry price for PMS has moved toward the upper bound of ₦1,175 to ₦1,250 per litre. To provide immediate relief, the government could temporarily pause regulatory taxes from 47 government agencies, which are estimated to inflate gantry prices by ₦101-₦120 per litre. By removing this “agency friction,” the state can facilitate a lower pump price without resorting to the blunt, distortive tool of consumption subsidies, thereby preserving the structural reforms of the last two years.

Monetary Policy: The CBN’s Tightrope Walk

The Naira has shown remarkable resilience in the first quarter of 2026, trading at a year-to-date average of ₦1,386/$ in the official window as at 13 March 2026. This stability is supported by a 13-year peak in foreign reserves, which reached $50.03 billion on 11 March 2026. However, the Middle Eastern shock threatens to undo this hard-won progress. The Central Bank of Nigeria (CBN), under the “Cardoso Doctrine” of orthodox inflation targeting, had commenced a gradual easing cycle, trimming the Monetary Policy Rate (MPR) to 26.5% in February 2026. However, the geopolitical shock has forced an immediate rethink. A “Major Escalation” would pressure the Naira through increased import costs for machinery and chemicals. To prevent a violent inflationary reversal, the CBN must remain prepared to pivot back to a hawkish stance, potentially raising the MPR to 27% or higher to mop up excess liquidity and defend the currency against speculative attacks.

Debt Dynamics: The Cost of Capital Shock

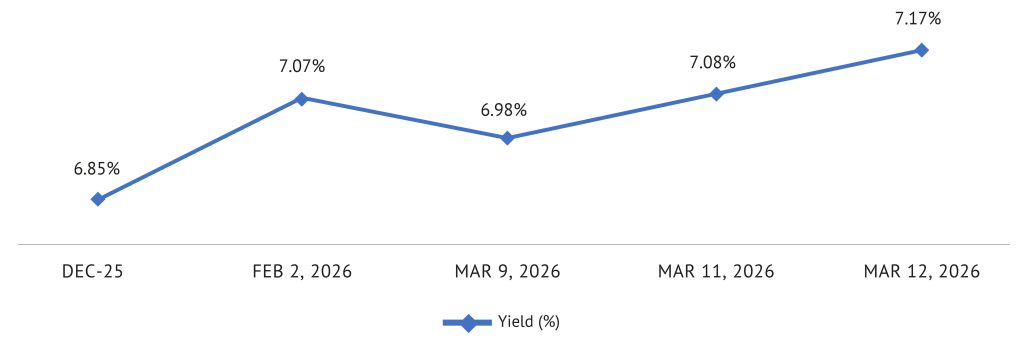

A critical dimension of the 2026 outlook is the impact of geopolitical tension on Nigeria’s sovereign debt profile. As global investors flee to “Safe Haven” assets, yields on Nigerian Eurobonds have seen a sharp uptick. In early March, the average yield on Nigeria’s Eurobonds rose 19 basis points (bps) to 7.17% as risk premiums expanded across the frontier market basket.

Figure 3: Average Eurobond Yield (%)

Sources: Debt Management Office (DMO), Bloomberg

For the Ministry of Finance, this represents a significant structural hurdle. The 2026 Medium-Term Expenditure Framework (MTEF) relies on successful external borrowing to fund the ₦15.5 trillion deficit. With global liquidity drying up, Nigeria faces a “Cost of Capital” shock. The debt-service-to-revenue ratio, officially projected at 74.3% in 2026, remains hypersensitive to any sustained Naira depreciation, making fiscal consolidation a moving target.

Social Stability: The “Fragility Trap”

Beyond the technicalities of monetary policy lies the most volatile variable: social stability. In Nigeria, fuel costs are the primary driver of logistics and food prices. With petrol already breaching the ₦1,300 threshold in some parts of the country, the impact on staples like rice and maize will be near-instantaneous. For a population spending over 60% of household income on food, this creates a “fragility trap.” The Nigeria Labour Congress (NLC) has already signalled that these price levels represent a “red line” for industrial action. Policymakers are now faced with a binary choice: allow market forces to clear at the risk of civil unrest or re-introduce “targeted relief” that would bleed the fiscal windfall from oil. In this high-stakes environment, the pressure to revert to populist subsidies is overwhelming, potentially undermining Nigeria’s hard-won fiscal credibility.

Conclusion: Beyond the Windfall – The Discipline of Survival

For Nigeria, the 2026 geopolitical reality is one of “Calculated Realism.” While the Middle Eastern cauldron offers a temporary fiscal lifeline through elevated crude prices, history reminds us that for a production-stunted economy, a price windfall is often a poisoned chalice. Without the institutional fortitude to meet the 1.84 mbpd output target, Nigeria remains a mere spectator to its own potential prosperity.

To navigate this high-tension era, policymakers must pivot from reactive crisis management to a proactive triad of discipline: accelerating “Crude-for-Naira” arrangements to secure upstream volume, maintaining a hawkish monetary firewall to protect the hard-won stability of the currency, and deploying surgical social safety nets that bypass the waste of systemic subsidies. This is in addition to establishing a transparent, rule-based mechanism to ringfence “excess” revenues. Unlike the opaque management of previous booms, we believe this windfall must be legally mandated for infrastructure de-bottlenecking and debt amortisation to break the cycle of fiscal profligacy. In the final analysis, Nigeria’s resilience in 2026 will not be determined by the price of oil in the Persian Gulf, but by the courage of its domestic policy choices. In a world of volatility, the only true hedge against external shocks is internal efficiency.