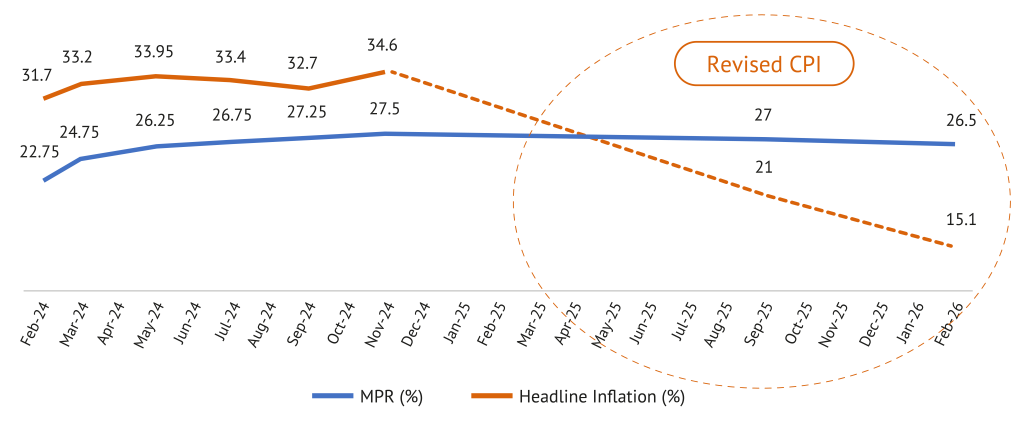

At the conclusion of its 304th statutory meeting on 24 February 2026, the Central Bank of Nigeria’s (CBN) Monetary Policy Committee (MPC) delivered a unanimous, albeit cautious, verdict on the nation’s monetary trajectory. By pruning 50 basis points off the Monetary Policy Rate (MPR) – bringing it to 26.5% – the Committee signalled its second strategic retreat from a hawkish stance in just five months. Governor Olayemi Cardoso’s post-meeting briefing framed the aforementioned as a measured salute to eleven straight months of disinflation (albeit engineered), with the headline inflation easing to 15.1% in January 2026, from 15.15% in December 2025, and gross external reserves ballooning to a 13-year high of $50.45 billion (9.68 months import cover). Yet, the question for the astute observer is whether this easing cycle represents a genuine structural shift. With Brent crude clinging to $75 per barrel on Middle East jitters, a US Fed under new stewardship eyeing cuts from 4.25-4.50% amid President Trump’s tariff tsunamis, Nigeria’s policymakers tread a familiar tightrope – unshackled on paper, but subsidy ghosts and election fiscal largesse lingering.

The Disinflation Mirage and the Methodology Dilemma

The centrepiece of the MPC’s rationale remains the sustained deceleration in headline inflation. For a nation that spent much of 2024 and 2025 gasping for air under the weight of ravaging inflation – which peaked at a 28-year high of 34.8% in December 2025 – this decline appears to be a triumph of monetary orthodoxy. However, the institutional scepticism that characterises the Nigerian market remains unpacified. A significant portion of this ‘statistical victory’ is attributed to a change in inflation methodology – a move that, while perhaps technically sound, has left a lingering scent of ‘manufactured progress’ in the air. When a regulator changes the thermometer, it does not necessarily mean the patient’s fever has broken.

Figure 1: Headline Inflation (%) vs. MPR (%)

Source: CBN, National Bureau of Statistics

Of particular note was the month-on-month headline inflation figure, which plummeted to a staggering -2.88% in January 2026. To find a precedent for such a sharp contraction in price levels, one would have to look back to periods of profound economic paralysis. While the CBN credits the ‘lagged transmission’ of its previous hikes, a more sober analysis suggests that this deflationary impulse reflects a collapse in aggregate demand.

When the cost of basic staples like rice and beans has risen by over 120% in the last five years while the minimum wage (raised to ₦70,000 in 2024) has barely doubled, the resulting ‘affordability crisis’ has tempered consumption growth, contributing to demand moderation that can dampen price momentum, creating disinflation without necessarily signalling improved supply conditions or productivity expansion. In this context, the observed moderation in inflation may reflect, at least in part, consumption fatigue within a cash-constrained consumer base rather than a more productive economy, but rather the sound of a consumer base that has finally run out of cash.

The CRR-MPR Asymmetry: A Policy of Controlled Suffocation

The Committee’s decision to lower the MPR while keeping the Cash Reserve Ratio (CRR) firmly anchored is a sophisticated, if somewhat contradictory, piece of monetary engineering. By reducing the MPR to 26.5%, the CBN is signalling to the markets that the cost of capital should begin to descend. Yet, by locking away nearly half of the banking industry’s deposits in non-interest-bearing reserves, the central bank is ensuring that the actual volume of available credit remains severely restricted. This creates a liquidity bottleneck that effectively serves as a safety valve against the Naira’s volatility.

This policy reflects a deep-seated fear of “excess liquidity.” The Nigerian banking system is currently awash with cash, evidenced by the recent ₦3.5 trillion “mop-up” via the Standing Deposit Facility (SDF) at an eye-watering cost to the CBN’s own balance sheet. By retaining the Cash Reserve Ratio (CRR) at 45% despite the MPR cut to 26.5%, the CBN ensures banks remain “resource-constrained” in credit creation from deposits. The recent ₦4tn recapitalisation bolsters balance sheet resilience but does not expand lendable funds, leaving real sector credit availability as tight as ever despite easing headline borrowing costs.

The $50 Billion Fortress: A Golden Shield or a Paper Umbrella?

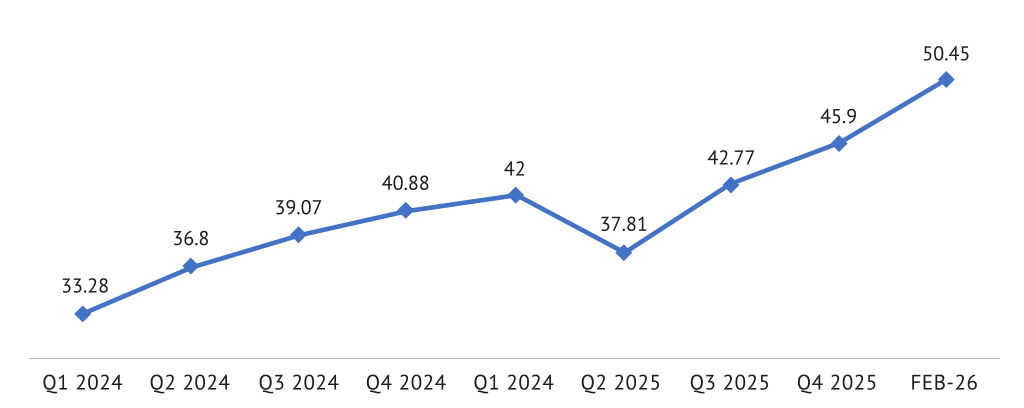

Perhaps the most potent narrative emerging from the February 2026 MPC meeting is the remarkable accretion to Nigeria’s gross external reserves, now standing at a 13-year high of $50.45 billion as at 16 February 2026. This fortress has been constructed through sustained oil export earnings, remittance inflows exceeding US$20 billion annually, and broader FX market stabilisation following unification reforms. The Monetary Policy Committee specifically welcomed the newly issued Presidential Executive Order 09, which mandates direct remittance of all oil and gas revenues into the Federation Account, noting its potential to further enhance fiscal revenue flows and reserves accretion by addressing longstanding leakages in Joint Venture (JV) profit oil allocations and Production Sharing Contract (PSC) deductions that historically bypassed transparent FX streams.

However, the quality of these reserves is as important as the quantity. A substantial portion of this growth has been driven by invisible flows – remittances and, more crucially, foreign portfolio investors (FPIs). These investors have been lured into the Nigerian market by some of the highest real interest rates in the emerging world. As the CBN begins to cut rates, the ‘carry trade’ that has supported the Naira becomes less attractive. If the interest rate differential between the naira and the US Dollar narrows too quickly, this $50 billion shield could prove to be a paper umbrella in a storm of capital flight. The Governor’s emphasis on ‘invisible flows’ is a tacit acknowledgement that Nigeria’s stability is currently rented, not owned. Until the nation can replace FPI with sustained Foreign Direct Investment (FDI) in productive sectors – which have been neglected during the high-interest-rate era – the reserves remain a hostage to global risk appetite.

Figure 2: Gross External Reserves (US$’ Billion)

Source: The CBN

The Washington Shadow and the New Fed Paradigm

Nigeria’s monetary pivot is being executed under the long shadow of a shifting paradigm in Washington. The emergence of a new United States Federal Reserve Chairman has introduced a period of profound uncertainty for emerging markets. As the US Fed recalibrates its own path towards a ‘neutral’ rate, the global competition for capital is intensifying. If the US Fed remains ‘higher for longer’ to combat its own persistent inflationary pressures, the pressure on the naira is likely to intensify. The Nigerian authorities must recognise that they are not just competing with their own historical performance, but with a US Dollar that remains aggressively attractive to global yield-seekers.

Furthermore, the geopolitical chessboard in the Middle East poses a direct threat to the fiscal assumptions underlying the CBN’s optimism. Ongoing peace negotiations involving Iran suggest that a significant volume of sanctioned crude could soon return to the global market. Projections of oil prices potentially sliding towards the $60 per barrel mark by Q4 2026 have already been articulated by Goldman Sachs. For a Nigerian economy that has only just begun to benefit from the Dangote Refinery’s impact on the balance of payments, such a price collapse could be devastating. A lower oil price would not only shrink the federation’s revenue but would also force the CBN to choose between defending the naira or allowing the reserves to bleed. The 50-basis-point cut is therefore a ‘fair-weather’ policy; should the global oil market turn sour, the Committee may find itself making a U-turn before the year is out.

Election Jitters and the Spending Spree

While the CBN has played its part in the ‘disinflation narrative,’ the greatest threat to price stability remains the fiscal side of the house. Nigeria is rapidly approaching the campaign season for the 2027 general elections. Historically, election cycles in Nigeria are marked by a total abandonment of fiscal discipline. The MPC communiqué explicitly identified ‘increased fiscal releases’ and ‘election-related spending’ as the primary ‘upside risks’ to the inflation outlook. The CBN Governor’s recent public statements – widely regarded as “open mouth operations” – have underscored profound concern over the anticipated “spending spree” during the forthcoming election cycle. If the political class pumps trillions of naira into the system to secure electoral advantages, the 11-month disinflationary trend will be reversed almost overnight. This creates a ‘tug-of-war’ between a central bank trying to cool the economy and a government trying to heat it up for political gain. For investors, the precarious equilibrium of 15% inflation and 4.5% GDP growth is a fragile consensus that could be shattered by the first wave of election-related liquidity. The ‘independence’ of the apex bank will be put to its ultimate test in the coming eighteen months, and historically, the fiscal side has rarely lost such a contest in Nigeria.

Market Implications: Navigating the Yield Peak

For the institutional investor, the message from the February 2026 MPC meeting is one of diminishing returns on fixed income. The era of the ‘yield peak’ in Nigeria has clearly passed. The massive over-subscription of the recent FGN Bond auction – where the market offered ₦2.7 trillion against an ₦800 billion target – shows that the smart money is already scrambling to lock in high yields before the easing cycle accelerates. As the MPR continues its descent, we expect a gradual rotation of capital towards the Nigerian Exchange (NGX), which, as at 25 February 2026, has already seen a 26% year-to-date appreciation. However, this migration must be tempered with caution; the “sticky” nature of core inflation and the looming election risk suggest that the stock market’s bull run could be vulnerable to sudden corrections.

The Verdict: A Sovereign High-Wire Act

In the final analysis, the CBN’s February 2026 decision is a masterclass in defensive easing. It is an attempt to find a “sweet spot” – a rate that is high enough to keep the naira stable and the FPIs interested, but low enough to prevent the economy from slipping into a deeper malaise. The 50-basis-point cut is a “signal of intent,” not a “declaration of victory.” The outlook for the remainder of 2026 is one of “guarded optimism.” If the CBN can maintain its “evidence-based” framework, and if the fiscal authorities can resist the siren song of election-year profligacy, Nigeria may finally be on the path to sustainable growth. The message to the market is clear: the peak of the crisis has been summited, but the descent toward a stable, low-inflation environment requires continued vigilance and a refusal to succumb to complacency. The outlook for Easter and beyond remains positive, but in the volatile world of 2026, the only certainty is the need for an evidence-based and adaptive policy framework.