On 1 May 2026, the global energy landscape underwent a definitive realignment that few in the traditional diplomatic circles of Vienna cared to publicly acknowledge. The formal withdrawal of the United Arab Emirates (UAE) from the Organisation of the Petroleum Exporting Countries (OPEC) is a development that signals the end of an era defined by managed scarcity and the beginning of a period of hyper-competitive energy realism. While the cartel has navigated the exits of marginal producers in the past, the departure of its most technologically advanced and fiscally ambitious member represents a fundamental challenge to the institutional logic of collective price management. As Abu Dhabi uncouples its production trajectory from the constraints of the Riyadh-led consensus, the global oil market must confront a reality where national strategic autonomy has finally superseded the “Vienna Consensus.”

The Institutional Lifecycle: From Sovereign Guard to Cartel Fatigue

To appreciate the gravity of the current moment, one must look past the immediate market volatility and revisit the institutional foundations of OPEC. Established in 1960 in Baghdad, the organisation was a revolutionary act of resource nationalism. Its primary objective was to wrest control of pricing and production from the “Seven Sisters” – the Western oil majors that had dictated the terms of trade for the first half of the 20th century. For decades, OPEC functioned as a geopolitical vanguard, most effectively during the 1973 embargo, asserting producer-country sovereignty and fundamentally altering the global distribution of wealth.

However, the cohesion of any cartel is a function of shared interests and external threats. In the 20th century, the threat was Western corporate dominance. In the 21st century, the threat is two-pronged: the technological disruption of U.S. shale and the existential pressure of the global energy transition. The creation of OPEC+ in 2016 was a tactical expansion designed to include Russia and maintain market relevance. Yet, this expansion introduced deeper internal contradictions. The “OPEC+ era” has been defined by a growing tension between members with high fiscal breakeven points who require high prices today, and those with massive low-cost reserves who seek to defend long-term market share. The UAE has now concluded that the price-support benefits of membership no longer justify the opportunity cost of idling its vast capacity.

The ADNOC Imperative: Why Abu Dhabi Walked

The UAE’s decision is the culmination of a decade-long transformation of the Abu Dhabi National Oil Company (ADNOC). Under its current leadership, ADNOC has moved from being a traditional state-owned operator to a high-efficiency global energy major, more akin to a diversified multinational than a government department. This shift was supported by a $150 billion capital expenditure programme aimed at scaling production capacity toward 5 million barrels per day (mbpd).

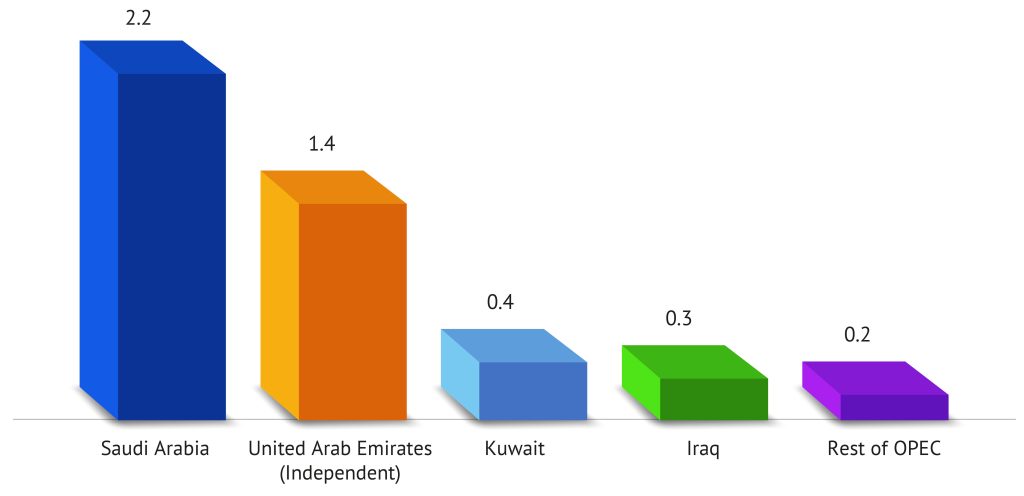

Under the previous OPEC+ framework, the UAE was frequently restricted to a quota of circa 3.5 to 3.6 mbpd. This meant that approximately 30% of the UAE’s invested capital was effectively rendered unproductive by diplomatic agreement. In the high-price environment of early 2026, the fiscal loss of leaving nearly 1.4-1.5 mbpd underground became an untenable burden. Furthermore, Abu Dhabi has adopted a “first-mover” logic regarding the energy transition. As global electric vehicle (EV) adoption and renewable scaling accelerate, the window for hydrocarbon relevance is narrowing. Abu Dhabi’s strategy is built on the belief that it is better to produce and sell as much as possible now, while demand remains robust, rather than risk holding stranded assets in a decarbonised 2040. This “monetise-now” philosophy contrasts sharply with the Saudi “market-steward” approach, which seeks to prolong the life of the oil era through careful price management.

Figure 1: The Stranded Capacity Gap (UAE Focus), mbpd

Source: OPEC

Institutional Fragmentation: A Terminal Structural Decline?

The UAE follows Qatar (2019), Ecuador (2020), and Angola (2023) out of the door. However, the exit of Abu Dhabi is analytically distinct. Unlike previous exits, which involved marginal producers or gas-centric economies, the UAE takes with it the cartel’s most reliable source of incremental production. This challenges the very definition of OPEC. We are witnessing its evolution from a traditional price-management cartel into a looser coordination platform. Without the UAE’s compliance, the burden of market balancing falls almost entirely on Saudi Arabia and Kuwait.

This creates a “Free-Rider” problem: if Saudi Arabia cuts production to support prices, the UAE – as a “free agent” – can simply fill the gap and capture the revenue. Historically, such asymmetric burdens are unsustainable and often precede “market-share wars” where the dominant producer floods the market to punish non-compliant peers. For global traders, the disappearance of the OPEC discipline premium means that a permanent “volatility premium” is now the new normal. The institutional cohesion that once allowed OPEC to act as the “central bank of oil” has been permanently compromised.

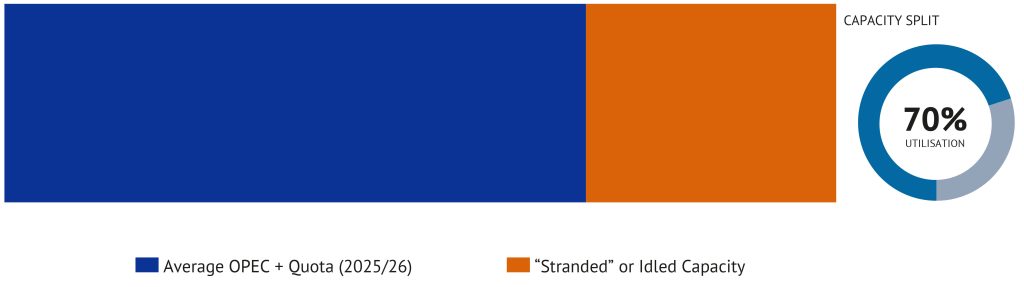

Figure 2: OPEC’s Estimated Spare Capacity (mbpd)

Source: OPEC

The Nigerian Imperative: Fiscal Fragility in a Fragmented Market

For Nigeria, the UAE’s exit is not an abstract geopolitical event; it is a direct threat to the country’s fiscal stability. Nigeria represents the “vulnerable middle” of the oil market – a producer with high extraction costs ($25-$48 per barrel vs. OPEC+ average of $10 per barrel), ageing infrastructure, 83.8% of export receipts in 2025. The transmission mechanism from global oil prices to the Nigerian macro-economy is brutal and immediate:

Revenue Vulnerability and Budgetary Assumptions: The Nigerian 2026 fiscal framework is built on a delicate set of assumptions regarding oil price and volume. Any downward pressure on Brent crude caused by a UAE production surge, or a broader “market share war”, could trigger a significant revenue shortfall. With the country already grappling with an estimated ₦1.76 trillion loss due to missed production targets over the last 14 months, the fiscal authority has no buffer to absorb a price collapse. Nigeria’s debt sustainability is inextricably linked to oil revenue; lower prices would inevitably lead to a higher debt-service-to-revenue ratio, further crowding out essential infrastructure spending.

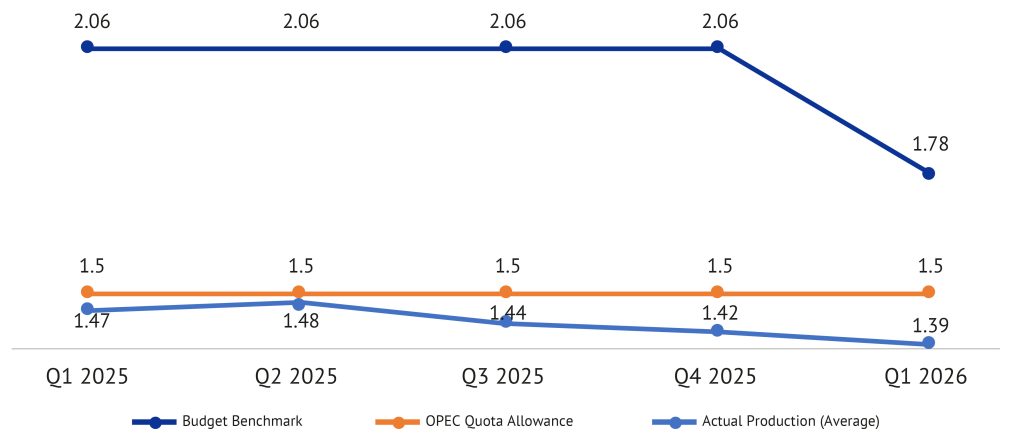

The Capacity-Quota Paradox: The tragedy of Nigeria’s position is that while the UAE left OPEC because its quota was too low, Nigeria has consistently failed to meet even its constrained allowance. In the first quarter of 2026 (Q 2026), Nigerian crude oil production averaged just 1.38 mbpd, well below the 1.5 mbpd allocated quota, largely driven by vandalism, crude oil theft and under-investment. Consequently, Nigeria is unable to benefit from the “production flexibility” that a weaker OPEC might offer. Nigeria remains a “price taker” with a constrained volume base – the most dangerous position in a competitive market.

Figure 3: Nigeria’s Crude Oil Production – Quota vs. Reality (mbpd)

Source: OPEC MOMR, Budget Office of the Federation

Macroeconomic Transmission and Policy Risks: A fractured OPEC increases the likelihood of oil‑price volatility, which transmits directly into exchange‑rate pressure on the Naira. In March 2026, at its 304th Monetary Policy Committee (MPC) meeting, the Central Bank of Nigeria (CBN) lowered the Monetary Policy Rate (MPR) by 50 basis points, signalling a deliberate pivot towards growth‑supportive monetary policy. However, if oil revenues weaken further, Nigeria’s foreign‑exchange reserves are likely to face renewed stress, potentially forcing the CBN into a defensive tightening cycle that would partially offset the benefits of recent macroeconomic reforms. In such a scenario, higher fuel and energy costs, driven by a depreciating Naira, would further amplify headline inflation, steadily eroding the purchasing power of the Nigerian middle class.

The Competition for Asian Market Share: The UAE’s exit will lead it to aggressively target Asian markets, specifically India and China, which are the primary buyers of Nigerian “Sweet” crude. As ADNOC offers more competitive pricing and reliable supply, Nigeria risks being “crowded out” of its most important export markets. Without the protective umbrella of OPEC quotas to restrain competitors, Nigeria’s lack of competitiveness becomes a glaring strategic liability.

The West, OPEC, and the Future of Energy Power

The relationship between OPEC and Western powers is also evolving. Historically, the West viewed the cartel with antagonism, using Strategic Petroleum Reserves (SPRs) and shale production to counter its influence. Today, however, the energy transition is creating a more complex dynamic. Western decarbonisation policies are weakening OPEC structurally in the long term, but they are also increasing the cartel’s short-term leverage due to underinvestment in non-OPEC supply. The UAE’s exit suggests that the traditional “West vs. OPEC” binary is breaking down. By becoming a “free agent,” the UAE can form deeper, bilateral energy security pacts with Western and Asian nations without being bound by the political consensus of the Riyadh-Moscow axis. This fragmentation of producer alliances serves Western interests by potentially lowering long-term prices, but it also increases the risk of market instability and supply shocks.

Conclusion: The Era of Energy Realism

The UAE’s exit from OPEC marks the transition from an era of managed energy security to one of energy realism. National strategies are now superseding the collective ideals of the 1960s. For the UAE, the future lies in being an agile, low-cost “energy super-major” that prioritises monetisation over diplomacy. For Saudi Arabia, the challenge is maintaining the relevance of a shrinking club without bearing an unsustainable fiscal burden.

For Nigeria and other high-cost producers, the message is sobering. The “OPEC shield” that once provided a floor for national revenues is thinning. In this new order, fiscal survival will not be determined by diplomatic negotiations in Vienna, but by the ability to fix domestic infrastructure, secure production assets, and diversify the revenue base. Gas, in particular, should figure prominently in Nigeria’s response. With the country sitting on an estimated 215.19 trillion cubic feet (Tcf) of proven gas reserves – among the highest in the world and the largest in Africa – the potential exists to turn hydrocarbons from a vulnerability into a transitional strength. That potential, however, will only materialise if policymakers and investors commit to the infrastructure needed to monetise that gas: pipelines, processing facilities, export terminals, and domestic‑power‑and‑industry‑demand anchors. Without such investments, the gas advantage will remain largely theoretical.

The era of the cartel is setting; the era of the sovereign competitor has begun. Those who cannot adapt to this hyper-competitive landscape will find themselves not just out of the cartel, but out of the market entirely.