A season of gloomy forecasts

The Covid-19 pandemic has dealt a huge blow to the global economy. What is fundamentally a public health crisis has led to economic recessions of historic proportions in several economies drawing comparisons with the Great Recession of this century and the Great Depression of the prior century.

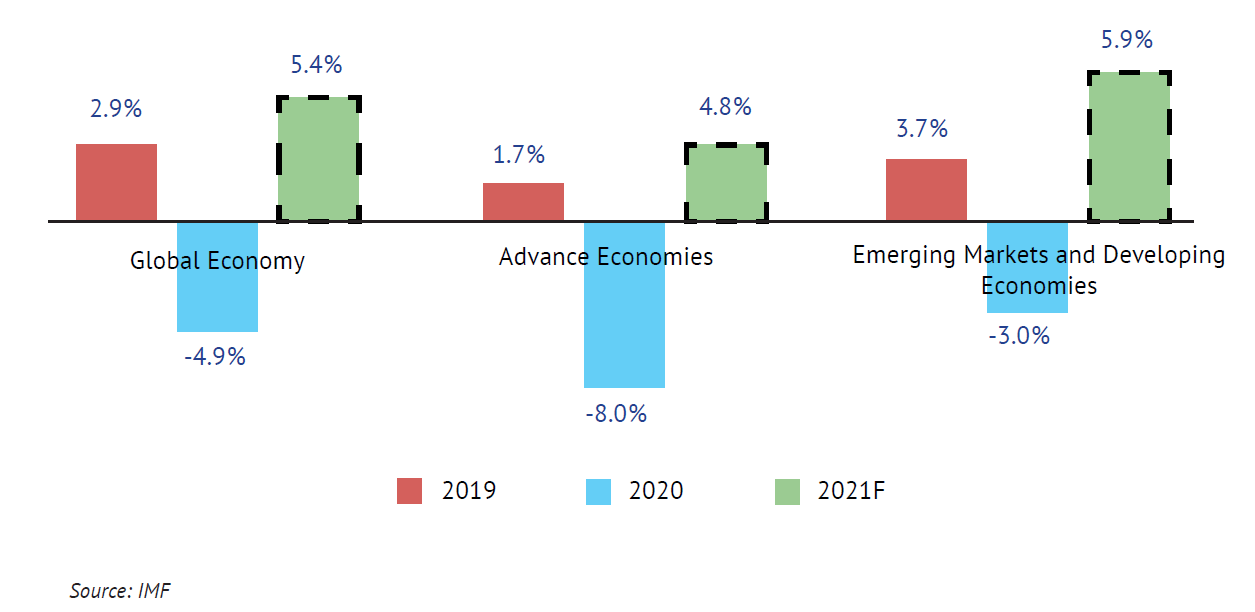

Estimates by the IMF in its June 2020 World Economic Outlook (WEO) forecast a sharp contraction of 4.9% in global output, with variations across different regions as advanced economies (AEs) are forecast to be the worst hit at -8% while emerging markets and developing countries (EMDEs) are forecast to witness a 3% decline. In the same vein, global demand for crude oil has tumbled – as economic activities retreated to a near halt due to lockdown measures imposed to flatten the Covid-19 curve – adversely impacting global crude oil prices. The severity of the shock in the crude oil market is reflected in the incidence witnessed during the early phase of lockdown where WTI crude nosedived into negative territory, trading at -$37 per barrel on April 20th, an occurrence which has understandably perplexed observers as it was never experienced in history.

According to data from the Budget Office, crude oil was about 62% of government revenues and 77% of export earnings in 2019. Thus, Nigeria has found itself grappling with a dual crisis – an oil crash and the pandemic with all its attendant economic ramifications.

Key Assumptions of Nigeria’s Revised 2020 Budget

Adjusting to the new reality, President Muhammadu Buhari signed the Revised 2020 Fiscal Budget into law on July 10, 2020, following several weeks of deliberations and negotiations with the National Assembly.

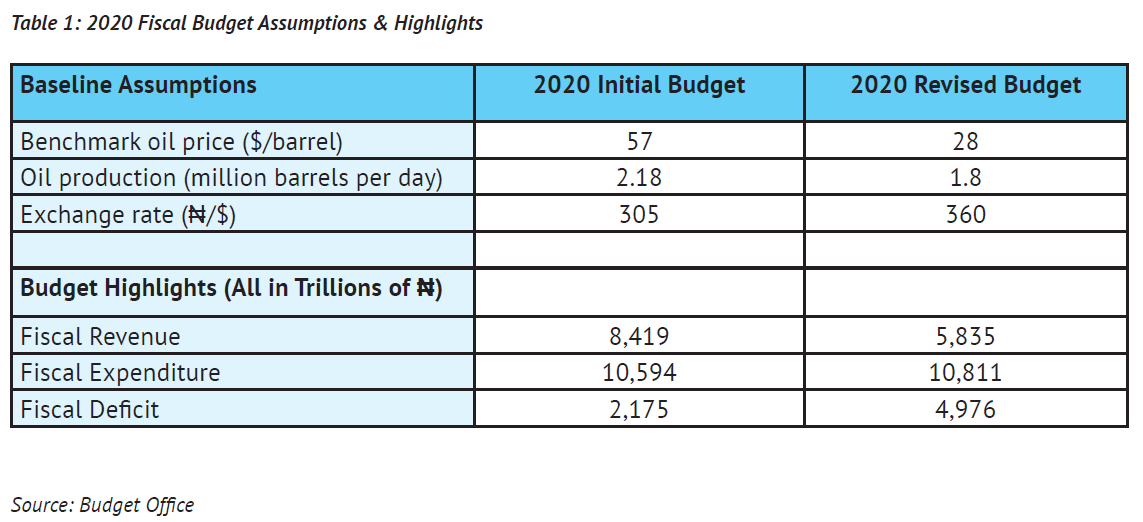

On the revenue side, adjustments were made to key parameters underlying the government’s revenue projections to reflect current global macroeconomic realities. Initially set at $57 per barrel, the oil price benchmark was revised downwards to $28 per barrel in the new budget. Oil production was equally revised downwards to 1.8million barrels per day (mbpd) from 2.18 mbpd due to the OPEC quota. The exchange rate was revised to ₦360/$ from ₦305/$ in line with the recent devaluation of the official exchange rate by the Central Bank of Nigeria (CBN). Consequently, overall fiscal revenue for 2020 is estimated at ₦5.84 trillion in the revised budget from ₦8.42 trillion in the prior budget reflecting a drop of 31%. The fiscal revenue estimates reflect oil revenue constituting approximately ₦1 trillion; tax revenues ₦1.6 trillion; and other revenue sources accounting for ₦3.2 trillion.

Playing it safe on the revenue side

Nigeria’s benchmark oil price of $28 per barrel in the revised budget falls well below oil price forecasts of other reputable global institutions for the rest of 2020, indicating the country’s fiscal authorities seem to be adopting a conservative approach on the revenue side. For instance, the World Bank is forecasting an average oil price of $35.4 per barrel and the US Energy Information Agency (EIA) has a price forecast of Brent Crude Oil price of $40.50 per barrel for the latter half of the year, reflecting a higher difference of 26% and 45% respectively on Nigeria’s price forecast. This material differential between Nigeria’s budget benchmark on crude oil and that of the World Bank and IEA reflects a conservative fiscal approach on revenues by the Nigerian authorities.

The Oil Markets

The revised budget is also hinged on an oil production volume of 1.8mbpd, an amount which is significantly above Nigeria’s 1.4million barrels per day quota (excluding condensates), as part of the latest OPEC+ agreement in April 2020. As part of measures to push prices higher, the OPEC+ cartel agreed to cut oil supply by 9.7 million barrels per day (representing 10% of global oil output) over the second quarter of the year in a move to stabilise the global oil market and mitigate the effects of low crude prices on their economies. At a time when the OPEC+ alliance member countries have demonstrated a high commitment in keeping to agreed production cuts – with compliance levels standing at a historic 85% in May – concerns around Nigeria’s non-compliance with the agreed quota during the second quarter of the year have surfaced. As per the OPEC+ alliance agreement, such non-compliance is to be subsequently sanctioned with a commensurate reduction in volumes. There have already been tentative talks by OPEC+ leaders and Nigerian authorities on the issue of compliance. Mele Kyari, the Head of Nigeria’s state oil company, the Nigerian National Petroleum Company (NNPC) conceded that the country had exceeded its quota in May 2020 due to technical challenges but aims to achieve full compliance by July. All these factors underscore the downside risks to Nigeria’s oil revenue target as set out in the revised budget.

On the flip side, the devaluation of the official exchange rate as reflected in the revised budget would translate into more revenues in local currency terms, thereby providing some revenue boost. With businesses clamouring for government support, consumer demand at a record low, and a slowdown in capital inflows, the prospects for non-oil revenues are dim. While the FGN has flagged-off the sale of 57 marginal oil fields through the Department for Petroleum Resources (DPR) in June 2020, swift execution of such an arduous process is very unlikely as it requires a dexterous balancing of competing interests and likely protracted negotiations. Already, certain regional interest groups including the Pan Niger Delta Forum (PANDEF) have aired their opposition to the plan, further stoking political risks. Accordingly, overall government revenues for the year are likely to fall significantly below the ₦5.84 trillion approved in the budget.

Expenditure profile of the revised 2020 fiscal budget

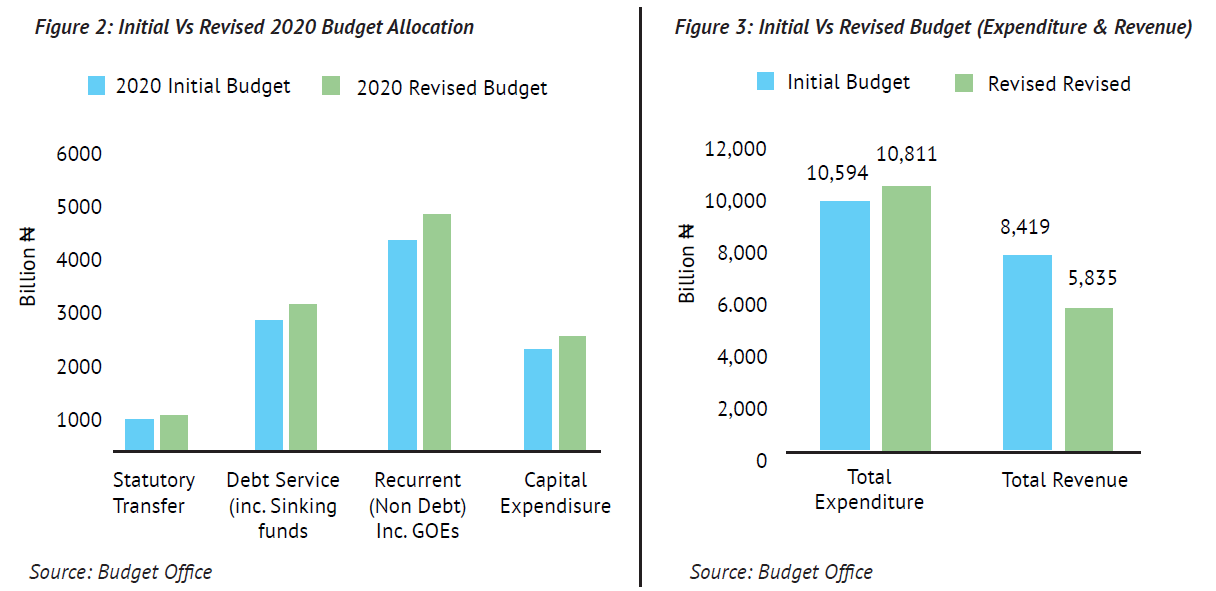

With aggregate spending of ₦10.8 trillion, the newly signed budget represents an upward revision to the tune of ₦216 billion compared to the initial budget in which aggregate government expenditure was set at ₦10.59 trillion. Statutory transfers receive an allocation of ₦428 billion; debt service (including sinking fund) is set at ₦2.95 trillion; recurrent (Non-debt) gets the highest allocation at ₦4.94 trillion and ₦2.49 trillion is earmarked for capital expenditure. The bulk of the increment within the new budget is channelled into recurrent spending and debt service – at ₦99 billion and ₦226 billion respectively, whereas capital expenditure receives a marginal boost of ₦23 billion and statutory allocation was revised downwards significantly.

The government projects a debt service to revenue ratio of 32%, and a capital expenditure to aggregate government spending ratio of 23%. Given the tight fiscal space, the former is an unrealistic projection, and the expectation is that debt service will gulp a substantially larger chunk of revenues. For context, debt service as a proportion of the Federal Government’s retained revenue was approximately 60% for the fiscal year 2019. Likewise, capital expenditure is expected to underperform severely, as the government only achieved a meagre 14% capital spending to aggregate expenditure in 2019.

In total, the increase in planned expenditure amidst the downward revision to revenues elevates the government’s projected deficit to GDP ratio to 3.57% – above the 3% guidance in Nigeria’s Fiscal Responsibility Act 2007. However, the Act allows the President to approve of a deficit ratio above the mandated ceiling in the event of a threat to the country’s sovereignty or national security.

Debt bingeing as a deficit financing tool

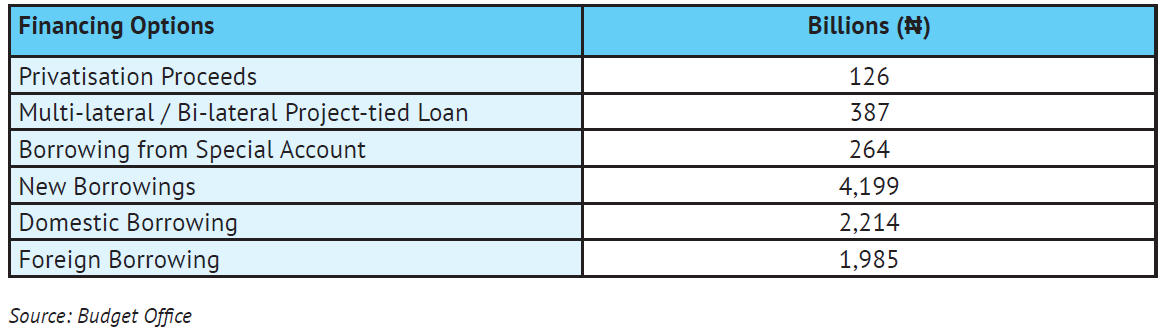

As the crisis lingers on, government continues to dig into various coffers to fund stimulus packages in a bid to resuscitate economic growth and provide some succour to households and businesses alike. For Nigeria, the coffers are fast depleting given minimal public savings and persistent budget deficits over the years without a concomitant improvement in fiscal revenue generation. The balance on the excess crude account (ECA), a national savings bucket where oil receipts above the benchmark set for the fiscal year are saved, stood at a meagre $72.4 million as of July 7, 2020. Similarly, funds available in the Stabilization Fund managed by the National Sovereign Investment Authority (NSIA), which are specifically earmarked to provide the government with a cushion during tough economic climes are too thin to significantly create a buffer to the wide fiscal deficit. Expected revenues from the privatisation of national assets – a plan which has been on the radar for years, are unlikely to be realised not least due to a lack of political will on the part of the government. With such low fiscal buffers, the government plans to finance the bulk of the ₦4.98 trillion deficit via a mix of foreign and domestic borrowings.

Table 2: Proposed Deficit Financing Options

Never too late to reform

As with past crises, the dual shock Nigeria is currently facing has laid bare some of the more fundamental pain points in the country’s economy. The confluence of a low, undiversified fiscal revenue base, a heavy central government that’s expensive to run, and structural bottlenecks all act to hamper public finances and national savings. In the near term, areas with the potential for cost savings within the government should be identified and be tapped into. While the revised budget gives the government the fiscal room to deliver much-needed palliatives to segments of the economy, its potency to provide a substantial boost to the macro-economy is weakened given the low expected revenues to deliver on the promise, the prioritisation of recurrent over capital spending, and the sheer depth of the 2020 recession, forecast at -5.4% by the IMF. At Agusto & Co. our forecasts across scenarios also signify a material contraction in GDP. While the base case scenario indicates a contraction of 4.5% in 2020, the worst-case scenario forecasts a GDP contraction of 7%.

It is pertinent that the Nigerian government embraces the crisis as a window of opportunity to push ahead with reforms that place the economy on a solid footing over the long run. Recurrent spending must be kept at bay, and productive capital expenditure, prioritized. However, with public finances stretched, it is the latter that gets relegated due to the political expediency of the former. To highlight this, the performance of the capital budget stood at 29% in the first quarter of the year, whereas recurrent spending of ₦2.09 trillion exceeded the prorated amount during the period by 16%. Although President Buhari has affirmed that all Ministries, Departments, and Agencies (MDAs) will be allocated 50% of their capital allocation by the end of July, the trend in fiscal spending priorities in the first quarter of the year is expected to be maintained as the year progresses.

The outlook for the Nigerian economy in 2020 looks bleak – as is the case with other countries across the globe. However, Nigeria’s fiscal response to the pandemic, as reflected in the newly revised budget, does little to reflate the economy and pivot the country toward a more resilient path once this pandemic is over.

Lessons for Nigeria

Overall, lessons from the rich world, and even the low-income countries offer important lessons to Nigeria on economic recovery in this pandemic. By escaping the worst of the pandemic through an effective healthcare response that pruned down the contagion and combining this with ambitious fiscal stimulus programs, New Zealand and Germany have effectively become the benchmarks for even their rich OECD peers.

On the other end, Bangladesh, a low-income Asian country, has responded effectively to the economic challenges of the pandemic in two major ways. Firstly, by channelling assistance from international institutions into priority areas such as social security and healthcare which has helped boost the country’s economic resilience and also promoting inclusive growth. Secondly, by reining its fiscal deficit – prior to the pandemic – Bangladesh has been able to create vital policy space for an effective pandemic response with a GDP forecast growth of 3.8% in 2020 and 6% in 2021.

Nigeria has vital lessons to learn from Bangladesh. The reward for fiscal discipline is a strong economic growth even amidst the pandemic. And the consequence for fiscal indiscipline is lethargic growth or in Nigeria’s case another recession in just four years, thus creating a pattern of economic omens in leap years.