Asset tokenisation is a transformative concept that emerged in the early 2010s alongside blockchain technology – a decentralised system that allows for secure and transparent sharing of information across a network of interconnected blocks. This innovative process involves converting tangible or intangible assets into digital tokens on a blockchain network, creating a digital representation that facilitates trade and management more efficiently.

Tokens (digital assets) can represent physical assets like real estate or art, financial assets like equities or bonds, intangible assets like intellectual property or even identity or data. Tokenisation can take various forms. A popular example is stablecoins – cryptocurrencies pegged to real-world currencies designed to be fungible (interchangeable). Examples include USDT (pegged to the US Dollar) and cNGN (pegged to the Nigerian Naira). Conversely, Non-Fungible Tokens (NFTs) are unique tokens representing ownership of scarce digital items that cannot be replicated – such as art.

In today’s world, some of the most popular use cases of real world assets (RWA) tokenisation can be found in real estate assets with a popular example being the St. Regis Aspen Resort, a luxury hotel in Colorado that sold 18.9% ownership as tokens for $18 million in 2018. The St Regis Aspen transaction is also unique in that it combines asset tokenisation with traditional real estate investment option – real estate investment trusts (REITs), whereby the tokenised portion of the asset is formed as a single asset REIT and each token will represent an indirect ownership of the stock (the St Regis Aspen). According to the asset owner, the REIT provides a tax-efficient structure for the transaction.

The Argument for Asset Tokenisation

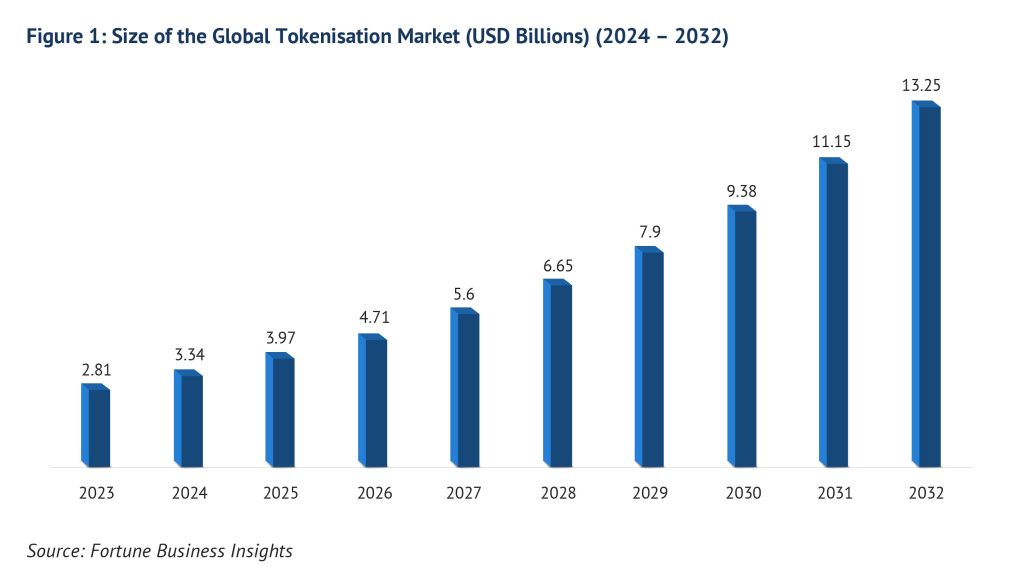

Despite impressive growth in assets under management (AUM) within global private markets – totalling $11.7 trillion in 2022, up from $7.4 trillion in 2020, and projected to reach $18 trillion in 2027 – alternative investments continue to face high barriers to entry, are expensive to fundraise, lack transparency and liquidity and remain inaccessible to many investors. Tokenisation addresses these challenges by utilising decentralised networks built on blockchain technology that allow remote verification of investors while broadening access to tokenised assets for anyone meeting the platform’s requirements. Larry Fink, CEO of BlackRock, emphasised this potential when he stated in January 2024: “We believe the next step going forward will be the tokenisation of financial assets, and that means every stock, every bond… will be on the general ledger.” Notably, BlackRock launched its first tokenised fund, BUILD on the Ethereum Network in March 2024 – a fund that invests 100% of its total assets in cash, U.S. Treasury bills and repurchase agreements.

How does Asset Tokenisation Work?

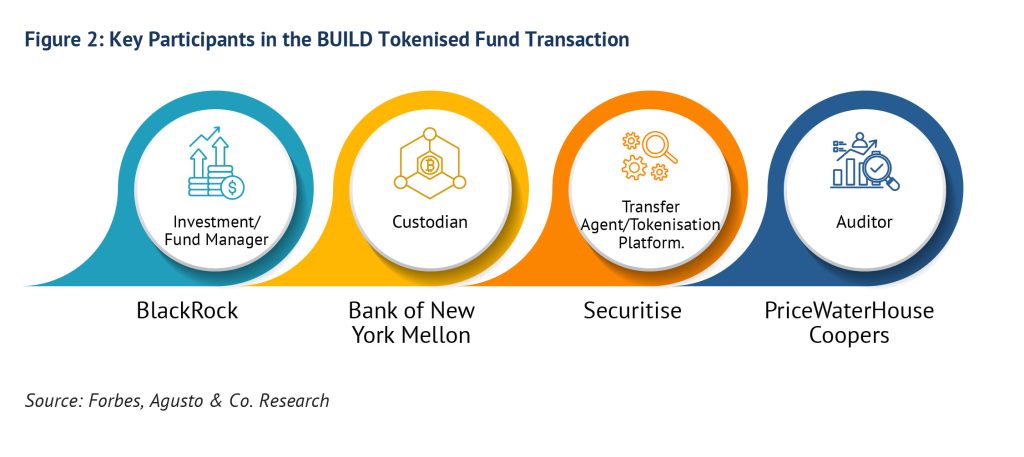

Although regulatory frameworks and asset peculiarity may determine the structure of asset tokenisation transactions, we believe most asset tokenisation transactions would involve the following parties:

- Investment/Fund Manager: which refers to the organisation who originally owns the assets to be tokenised and has initiated the tokenisation transactions.

- Custodian: which refers to the organisation that is responsible for maintaining and administering the real world assets during the lifetime of the tokenisation transaction. The responsibility for “housing” and managing the real world assets is transferred from the fund manager to the custodian following the initiation of a tokenisation process. This is done to maintain optimum transparency and safeguarding of assets.

- Tokenisation platform/Transfer Agent: This platform is responsible for managing the tokenised shares (assets) and reporting on fund subscriptions, redemptions and distributions. This platform is also where intending investors will buy and sell the tokenised assets.

- Auditors: The role of an auditor largely represents a regulatory requirement, and this role is generally supervisory with the aim of maintaining compliance to regulatory standards.

- Other financial market participants like credit rating firms will also play key roles in ensuring the validity and building credibility for tokenised assets. This would typically be in the rating on the underlying real world assets as well as the monitoring (rating) of the tokenised assets as it is done for bond issuances.

Using BlackRock’s BUILD Tokenised Fund as a case study illustrates these roles effectively:

Potential Benefits of Tokenisation for Financial Services Providers

Asset tokenisation offers several significant advantages for financial services, primarily through faster transaction settlements, democratised access, and enhanced transparency. By leveraging blockchain technology, asset tokenisation enables instant settlements that traditionally take two business days to complete, resulting in substantial savings for financial firms operating in high-interest environments and improving customer satisfaction. Furthermore, the simplification of operational processes allows financial services providers to effectively serve smaller investors, making it economically viable to cater to a broader audience. In addition, smart contracts – self-executing agreements coded into tokens – automate asset transactions securely and transparently, eliminating risks associated with manipulation found in traditional contracts. Overall, these features position asset tokenisation as a transformative force in the financial landscape, fostering greater inclusivity and efficiency.

Challenges and Considerations

Despite its advantages, asset tokenisation faces several challenges. Regulatory uncertainty presents a significant challenge in the realm of asset tokenisation, as the lack of consistent frameworks across jurisdictions creates confusion for investors and may hinder market growth. This inconsistency complicates compliance efforts and can deter potential participants from engaging with tokenised assets, leading to a reluctance to invest due to fears of regulatory repercussions. Additionally, cybersecurity risks are inherent in digital transactions; without robust security measures, investors remain vulnerable to fraud and data breaches, undermining trust in tokenised systems. Furthermore, a lack of understanding regarding technology-enabled solutions restricts participation among less tech-savvy individuals, potentially widening the financial inclusion gap.

The Potential of Tokenisation in Nigeria

For emerging markets like Nigeria, asset tokenisation also holds strong potential in various sectors offering innovative solutions to longstanding challenges. Unlike Real Estate Investment Trusts (REITs), which require investors to buy shares in companies owning income-generating properties – often subjecting them to management fees – tokenised real estate allows direct ownership stakes without intermediaries or additional costs associated with traditional REIT structures. In the commodities space, tokenisation can enhance liquidity and transparency by allowing fractional ownership of physical assets such as oil, gas, and agricultural products. This can attract a broader range of investors and facilitate easier trading on digital platforms. In agriculture, tokenisation can improve access to financing for smallholder farmers by enabling them to tokenise their produce or land, thus securing investments from a diverse pool of investors who may be hesitant to engage in traditional financing methods. This approach not only democratises access to capital but also enhances traceability and accountability in the agricultural supply chain. In addition, in infrastructure development, tokenisation can streamline funding processes by allowing for the creation of digital tokens representing shares in infrastructure projects. This can attract both domestic and international investors while reducing reliance on traditional funding sources, which often involve lengthy bureaucratic processes.

Conclusion

Asset tokenisation represents a significant evolution in how we view ownership across various asset classes – including within Nigeria’s dynamic economic landscape where opportunities abound amidst challenges faced by traditional systems today. By leveraging blockchain technology’s capabilities – to enhance liquidity & transparency while streamlining processes within financial markets – tokenisation paves the way forward towards more inclusive investment opportunities than ever before. Crucially, the Nigerian Securities and Exchange Commission (SEC), as the principal regulatory authority overseeing the capital market, has established comprehensive guidelines for the issuance and offering of digital assets. This initiative sets a significant precedent, which we believe will foster increased market interest in asset tokenisation. Complementing this regulatory framework, the NASD OTC Securities Exchange has launched its Digital Securities Platform (N-DSP), following SEC approval. This platform enables issuers to raise capital through digital assets and facilitates the trading and settlement of these assets, akin to the processes currently in place for traditional securities.

Furthermore, other prominent African economies, such as South Africa and Namibia, are actively embracing asset tokenisation. South Africa’s central bank is exploring the issuance of central bank digital currencies (CBDCs), while Standard Bank is delving into blockchain and tokenisation to revolutionise cross-border payments and trade finance. Namibia, on the other hand, has forged a significant $330 million partnership with DAMREV to tokenise a copper mine, marking a significant step forward in real-world asset tokenisation. These developments across Nigeria and other African nations illustrate a broader commitment to embracing innovative financial technologies that could reshape capital markets and enhance economic opportunities throughout the continent. As these trends continue evolving amid ongoing technological advancements & regulatory developments – the future looks increasingly promising for both Nigerian investors and global markets alike.