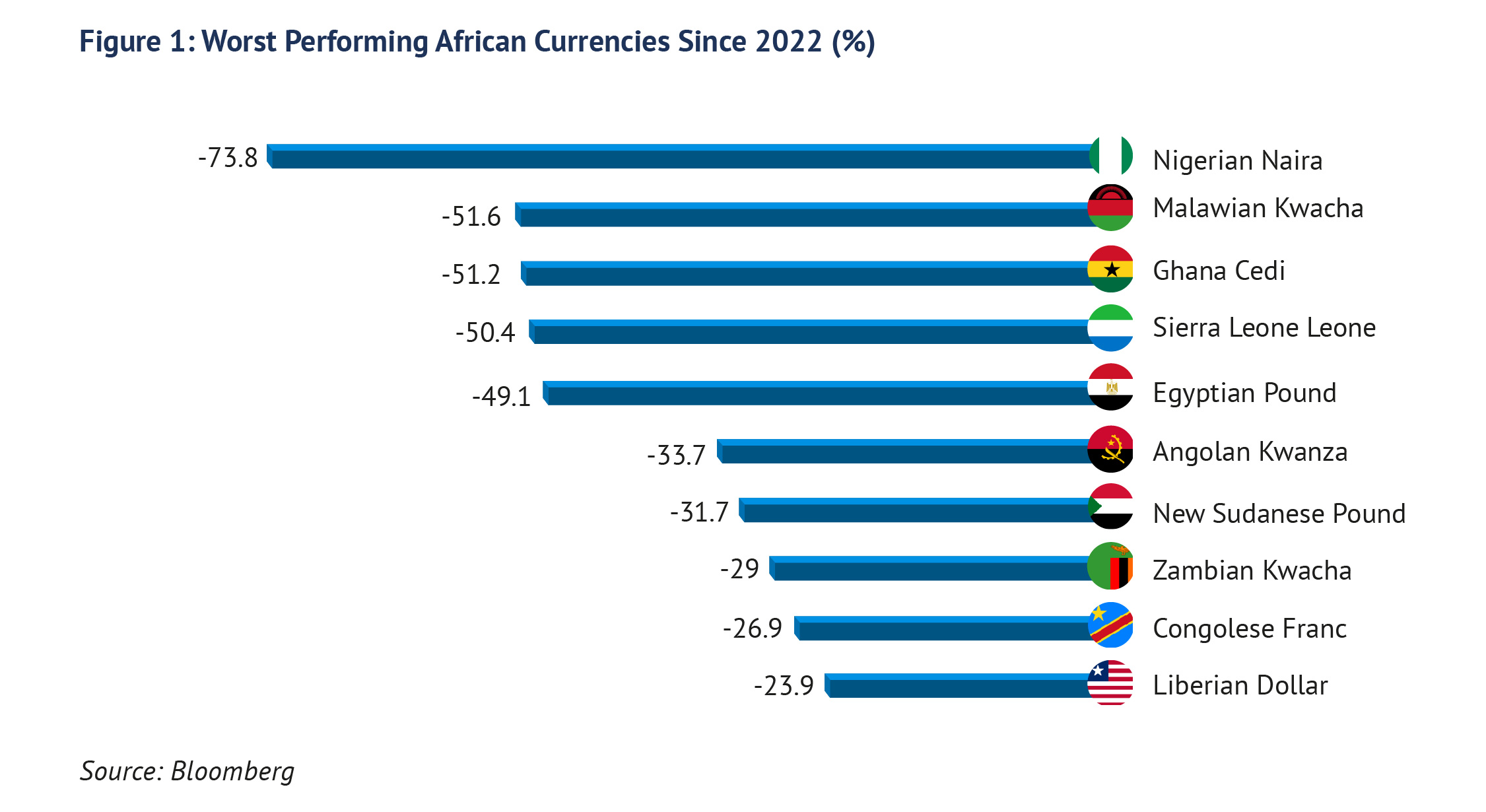

It is our position that the Central Bank of Nigeria’s (CBN) recent endeavors to stabilise the naira, following its plunge to an all-time low of ₦1900/$ at the parallel market on February 22 should ideally have preceded the decision to ‘float’ the naira. This observation clearly underscores the importance of timing considerations in the implementation of monetary policies for optimal efficacy and resilience as many believe that proactive measures could have potentially mitigated the severity of the naira’s precipitous decline since June 2023.

A semblance of stability has since been restored after a raft of policy directives geared towards addressing distortions in the foreign exchange (FX) market were issued, and the premium between the official and parallel market exchange rates declined further to 6% on the 5th of March from 25% on February 22nd. The CBN also heaped much of the blame for the naira’s free fall in recent weeks on speculative activity as it believes the naira is still undervalued and by instituting a fully functional FX market, which ensures free entry and exit, the currency will appreciate to a level that is consistent with fundamentals. Dr Cardoso, the CBN governor, alluded to this during a Foreign Portfolio Investor (FPI) call hosted by the Nigerian Exchange Group (NGX), where he left little room for ambiguity in his responses to questions on inflation and the exchange rate.

He reiterated the CBN’s dedication to maintaining price stability stating that the apex bank “will stop at nothing to tame inflation”, while also acknowledging the significant impact of the exchange rate pass-through effect on inflation, which reinforces the need for naira stability. By so doing, the CBN has acknowledged that it cannot sustainably tackle the exchange rate issue without first addressing inflation and, at the same time, it cannot tackle inflation without tackling the exchange rate. The CBN Governor emphasised that the focus for the exchange rate, is on fostering an environment that would place the naira firmly on a path of price discovery, moderation and stability, rather than just a fixed price. And therefore, during times of uncertainty, like the present, it aims to intervene and ensure as much stability in supply as possible.

Aggressive Measures and Cautious Optimism

In an effort to entice foreign investors, the CBN pledged to make rates more attractive for FPIs. He also announced plans to increase the frequency and volume of Open Market Operations (OMO). Following through on this commitment, the CBN successfully sold a record-breaking ₦1.053 trillion in one-year OMO bills, exceeding the initial offer of ₦355 billion by a factor of three. These bills were sold at a rate of 21.5%, translating to an effective yield of 27.3%. Notably, the CBN reported that nearly 80% of these bills were purchased by foreign investors, lured by the significantly higher yields. This robust participation can be interpreted as a positive sign for the CBN’s policy actions and a potential indication of gradually returning investor confidence in the Nigerian economy.

About 48 hours before the investor call, the Monetary Policy Committee (MPC) of the CBN hiked the Monetary Policy Rate (MPR) by an unprecedented 400 basis points (bps), raising it to a record-breaking 22.75% and increasing the Cash Reserve Ratio (CRR) from 32.5% to 45%, effectively tightening banking system liquidity. In addition, it adjusted the asymmetric corridor to a wider band of +100/-700 basis points, compared to the previous +100/-300. At the centre of its rationale is the current wave of inflationary and exchange rate pressures, and rising inflation expectations as it also believes that inflation will continue in its upward trajectory in the near term before hitting an inflection point and commencing a descent. These aggressive tightening measures reflect the CBN’s firm commitment to reining in inflation, curbing naira liquidity (currently at an all-time high of ₦93 trillion) attracting FX inflows and restoring exchange rate stability. The measures were welcomed by the IMF, at its End-of-Mission press release conveying its preliminary findings, after the completion of its 2024 Article IV Mission to Nigeria.

The Price of Stability

Tighter monetary conditions typically mean lower access to credit at higher costs. The response from Nigerian banks has been a 300-500 bps increase in lending rates (which is pegged to the MPR). Businesses and consumers may face difficulties obtaining loans due to tighter lending conditions, potentially dampening economic activity and investment. Existing borrowers, many of whom are already grappling with rising production costs, threatening their viability and competitiveness, are likely to see their loan repayments increase, putting additional strain on their finances and potentially leading to defaults. The disclosure by the Manufacturers Association of Nigeria (MAN) that, 767 manufacturers ceased operations, and 335 faced distress in 2023 is particularly worrying. This trend can be traced largely to exchange rate instability, escalating inflation, and broader economic challenges that have led to a significant deterioration in Nigeria’s investment landscape. Foreseeably, heightened borrowing costs are poised to exert additional pressure on the sector, exacerbating the accumulation of unsold finished products, which surged to ₦350 billion in 2023. This scenario unfolds against a backdrop of weakened consumption, as inflation bites deep, eroding purchasing power and squeezing household budgets.

The new CRR threshold places Nigeria far above its regional peers (South Africa: 2.5%, Kenya: 4.3% and Ghana: 15%). While Mr. Cardoso, at the investor call, committed to a gradual CRR mop-up so as not to shock the system, we believe that banks’ loan growth will be constrained in 2024 due to the increased procurement of treasury bills prompted by higher yields. The CBN now faces the task of proactively adopting a risk management perspective to navigate the implications of its newly adopted hawkish monetary policy stance on the banking sector.

The Imperative of Food Security

However, the IMF also noted that “…addressing food insecurity is the immediate priority…” This urgency is underscored by the spiraling food inflation at 35%, a figure many believe underestimates the true hardship faced by Nigerians. A confluence of factors, including lingering security challenges in food-producing regions, geopolitical and climatic factors, and the recent rise in energy and logistics costs following the removal of petrol subsidies, have all contributed to the significant increase in food prices. While addressing security concerns is essential to avert an impending food crisis, we believe a long-term solution lies in confronting the fundamental constraints hindering agricultural production. These constraints include low yields and inadequate storage and logistics infrastructure. Only by systematically addressing these issues can Nigeria sustainably increase food output and ultimately drive down prices for its citizens.

Beyond Monetary Policy: A Crossroads Awaits

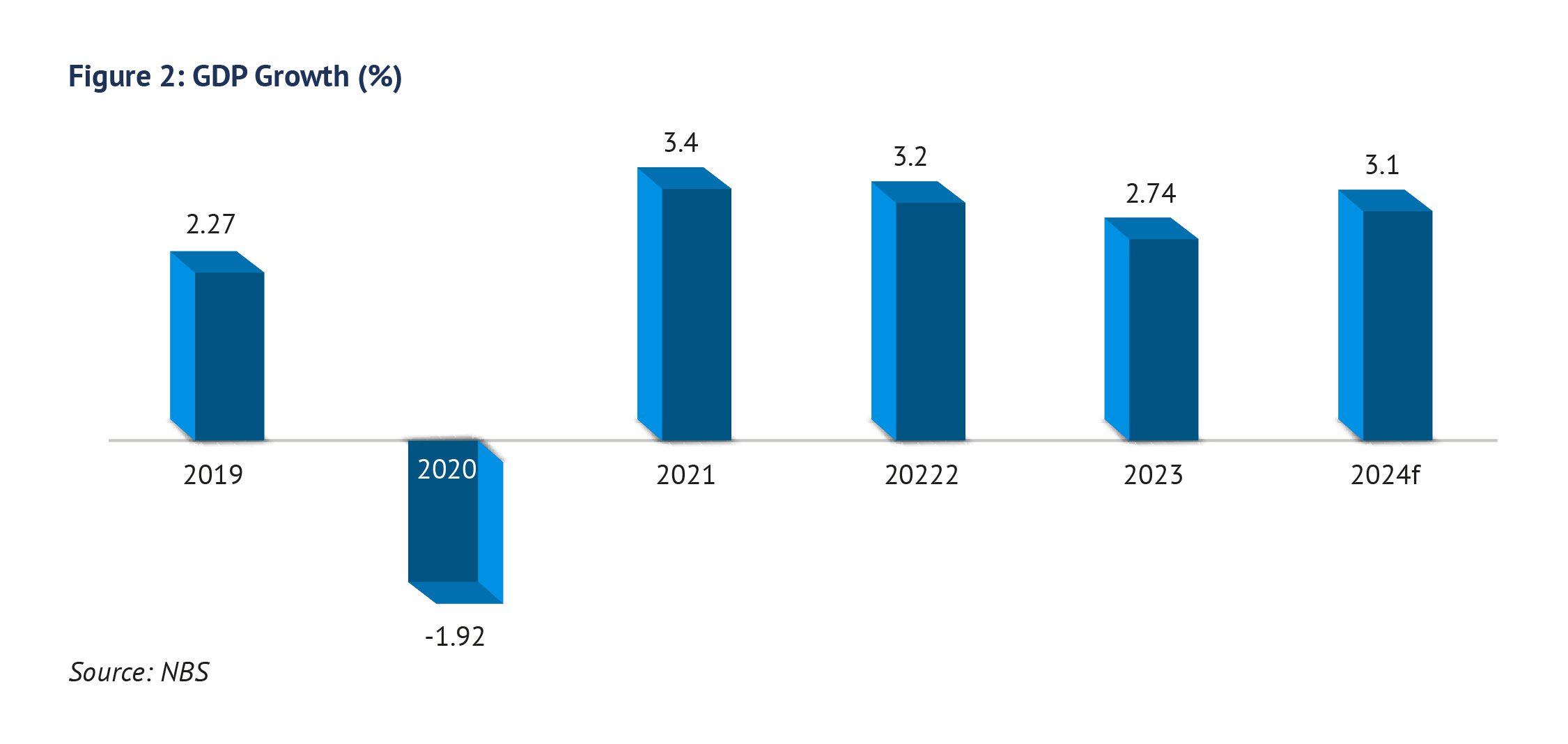

The Nigerian economy finds itself in a precarious position – stagflation. With GDP growth slowing for two consecutive years while inflation relentlessly climbs, decisive action is needed to boost output. We know that broad-based and sustainable GDP growth is only possible in a low-inflation environment while low output and productivity are significant structural inflation-stoking factors in Nigeria. Clearly, for the CBN, GDP growth considerations have taken a back seat and, as it should, the ball now rests squarely in the court of the fiscal authorities. Breaking this vicious cycle of inflation and low growth, requires structural reforms to support economic growth and mitigate the impact of monetary policy changes, while targeted interventions, investments in critical infrastructure, and promoting non-oil exports can foster diversification and resilience.

Governor Cardoso hinted at the possibility of the CBN clearing its foreign exchange (FX) backlog before the next Monetary Policy Committee (MPC) meeting on March 25th and 26th. While we acknowledge this is a necessary step, it’s insufficient for complete FX market stability. However, we believe clearing the backlog is crucial for strengthening public perception of the CBN’s reforms and potentially enhancing their effectiveness. The Nigerian economy stands at a critical juncture. While the CBN’s actions aim to address pressing economic concerns, their short-term impact might involve slower economic growth and tighter credit conditions. Navigating this complex situation demands a multi-pronged approach that combines effective monetary policy with complementary fiscal measures and structural reforms.