The Dissonance: Abuja vs. the Streets

Over the past three years, Nigeria has embarked on its most sweeping macroeconomic adjustment programme since returning to democratic governance. The core pillars have been unapologetically aggressive: the complete elimination of the premium motor spirit subsidy, stringent monetary tightening, fiscal consolidation, and foreign exchange market liberalisation. Evaluated strictly on the International Monetary Fund’s (IMF) orthodox scorecard, these reforms have delivered on their primary technical objectives. Macroeconomic stability has unequivocally improved, external buffers have been successfully rebuilt, and the sovereign’s access to international capital markets is thoroughly restored.

Yet this apparent success sits uncomfortably alongside deteriorating household welfare. Recent IMF surveillance concedes that poverty and food insecurity have worsened even as the headline indicators celebrated in Abuja and Washington have turned decisively upward. The result is a widening disconnect between an official narrative of stabilisation and the lived experience of households facing shrinking real incomes, erratic public services, and heightened insecurity. For policymakers, investors, and corporate decision‑makers, this gap is seeming increasingly like direct threat to the durability of the reform path and to the sovereign’s evolving risk profile, and is likely to test institutional credibility as the political calendar advances.

Global Liquidity, Local Illusions

The external environment offers little comfort. Despite Nigeria’s rebuilt reserves position and improved current account, global capital flows remain skewed towards advanced economies, where high policy rates and technology‑driven valuations (particularly artificial intelligence) continue to absorb vast pools of liquidity. For frontier markets, the promise of “renewed access” often translates into sporadic Eurobond issuance and volatile portfolio flows rather than the patient, bricks‑and‑mortar investment needed to transform infrastructure and industry.

Nigeria’s external statistics illustrate this tension. Export surpluses are driven largely by crude oil sales and import compression rather than a diversified, competitive export base. Non‑oil exports (27.4% of consolidated government revenue) remain narrow and vulnerable, constrained by logistics bottlenecks, power deficits, and regulatory uncertainty. Foreign investment flows, where they materialise, are dominated by short‑term portfolio money that stabilises the balance of payments but does little to deepen the productive base or generate employment at scale. In this context, higher reserves and an apparently comfortable current account do not automatically translate into tangible domestic gains. They function primarily as a defensive shield against external shocks and currency crises. That protection is significant, but it falls well short of the sort of capital formation required to shift the economy onto a higher, more inclusive growth path.

Stabilisation Gains: Stronger External Position, Weak Internal Transmission

The 2026 IMF Article IV report paints an economy entering a stabilisation phase. Real GDP growth was estimated at 3.87% in 2025 and is projected to reach 4.1% in 2026, supported by agriculture, real estate, information and communication technology, and oil. While 4.1% cannot dramatically transform a youthful, lower‑middle-income country with rapid population growth, it represents a distinct improvement over the preceding decade’s stagnation.

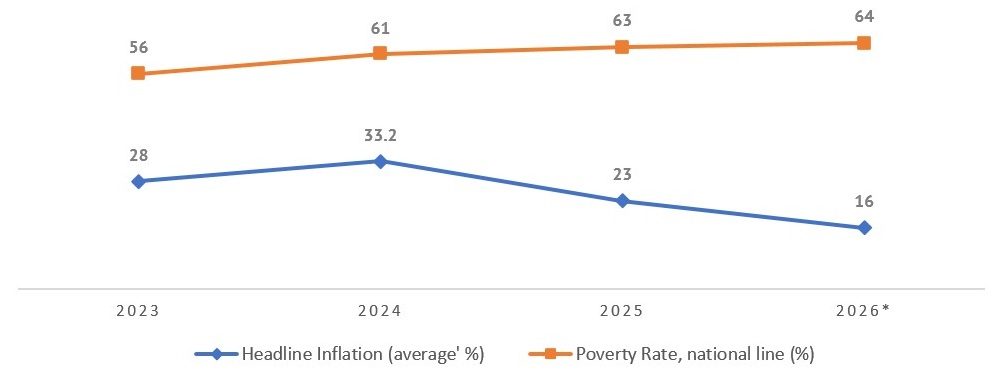

Inflationary pressures have shown signs of easing after reaching historical highs. Headline inflation, which spiralled to 34.8% in 2024, decelerated significantly to 15.06% in February 2026 before edging to 15.93% in May due to global commodity shocks. This disinflationary trend reflects a tighter monetary stance, foreign exchange stability following liberalisation, and improved domestic harvests. The Central Bank of Nigeria (CBN) is moving towards an explicit inflation‑targeting framework, positioning the policy rate as a clearer anchor for lending rates and inflation expectations.

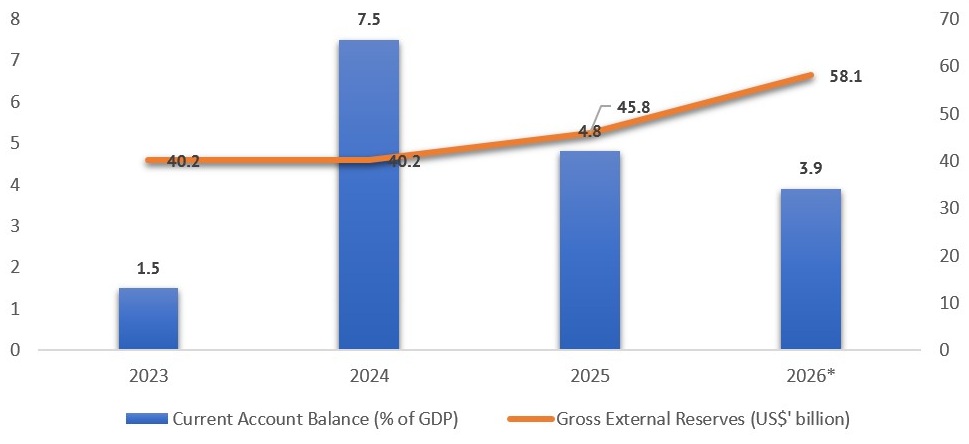

Simultaneously, external accounts have strengthened meaningfully. The current account registered a healthy surplus of 4.8% of GDP in 2025, underpinned by higher oil exports and reduced refined fuel imports. Gross external reserves rose to $45.8 billion by end-2025, supported by portfolio inflows and a successful $2.3 billion Eurobond issuance, and by June 2026, hovered at roughly $50 billion. and sustained current account support, the naira traded at around ₦1,370/$ in June 2026, representing an appreciation of c. 12% relative to its level in June 2025, demonstrating restored confidence in the reformed foreign exchange regime.

Figure 1: External Buffers and Current Account

Source: IMF, * = forecast

Regulation, Crowding‑Out, and the Credit Squeeze

Domestically, the Central Bank is aggressively tightening the regulatory perimeter around the banking sector, introducing structural shifts that carry unintended consequences for real economy lending. A recapitalisation exercise successfully raised ₦4.65 trillion (c. $3.4 billion) in new equity, with 33 of 37 commercial banks meeting revised requirements by March 2026. Financial authorities have advanced Basel III implementation, and investor sentiment is further supported by Nigeria’s removal from the Financial Action Task Force grey list.

However, the apex bank’s parallel implementation of stringent new guidelines for financial holding companies has fundamentally altered corporate banking behaviour. By forcing stricter capital buffers and mandating operational firewalls between core banking subsidiaries and holding parents, the regulator is attempting to insulate depositors from systemic shocks. In practice, this structural overhaul imposes a massive compliance tax. In a punitive interest-rate environment, these intense regulatory pressures risk suppressing credit creation. Adjusting for exchange rate valuation effects, the actual stock of domestic private sector credit remains low at about 12% of GDP. Commercial banks hold highly defensive portfolios, keeping roughly 22% of assets in safe, high-yielding government securities. The pension sector, valued at (₦27.45 trillion) 6.2% of GDP, is similarly overweight in government paper. This configuration creates a classic crowding-out effect, draining liquidity away from the private sector.

Broken Logistics, Stubborn Inflation

Nigeria’s chronic supply‑side weaknesses compound these financial constraints. The logistics backbone remains fragile, with underutilised rail capacity, congested ports, and deteriorating road networks. In practice, goods are forced onto overstretched road corridors, inflating transport costs and eroding any gains from currency stabilisation or moderating global commodity prices. This infrastructural decay feeds directly into the food and core inflation metrics the central bank is struggling to anchor. It represents an empirical demonstration of how broken execution at the state level directly undermines sophisticated macroeconomic modelling at the federal level. The central bank is using interest rates to restrain demand and attract capital inflows, consistent with its mandate to control inflation and support currency stability, while the true drivers of inflation are structural supply-chain inefficiencies that monetary policy cannot fix. The burden of adjustment falls entirely on productive corporate entities and vulnerable consumers, as high transport costs prevent the benefits of a stabilising currency from translating into lower retail prices.

The Microeconomic Reality: Distress Credit and Wealth Erosion

The human cost of this structural adjustment is explicit. Extreme poverty has swallowed roughly 63% of the population, and an estimated 27 million Nigerians faced severe food insecurity in late 2025. Pervasive insecurity continues to exact a heavy toll across agricultural belts, artificially depressing crop production. Crucially, the social protection response has been woefully modest relative to the colossal scale of the economic shock. By late 2025, roughly 9.2 million households were enrolled in a national cash transfer system, but received at maximum three isolated transfers of 25,000 naira ($18) each.

Figure 2: Inflation and poverty (%) – Diverging Paths

Source: IMF, World Bank, * = forecast

This severe pressure has triggered an alarming shift in financial behaviour. Within the middle and lower classes, the rapid rise of Buy Now, Pay Later structures is less a sign of consumer sophistication than of distress financing. As real disposable incomes are decimated, households leverage high-cost micro-credit simply to smooth daily consumption. For the urban middle class, the focus has pivoted from accumulation to defence. Deeply negative real returns on conventional savings instruments have pushed households (with estimated GDP per capita of $1,223 in 2025) towards informal hedges, ad hoc foreign‑currency exposures, and more active estate planning simply to preserve existing assets. When both poorer households and the middle class are orientated towards survival and capital protection rather than consumption and investment, aggregate domestic demand weakens, with direct implications for corporate earnings and tax receipts.

The Missing Social Compact and Fiscal Opacity

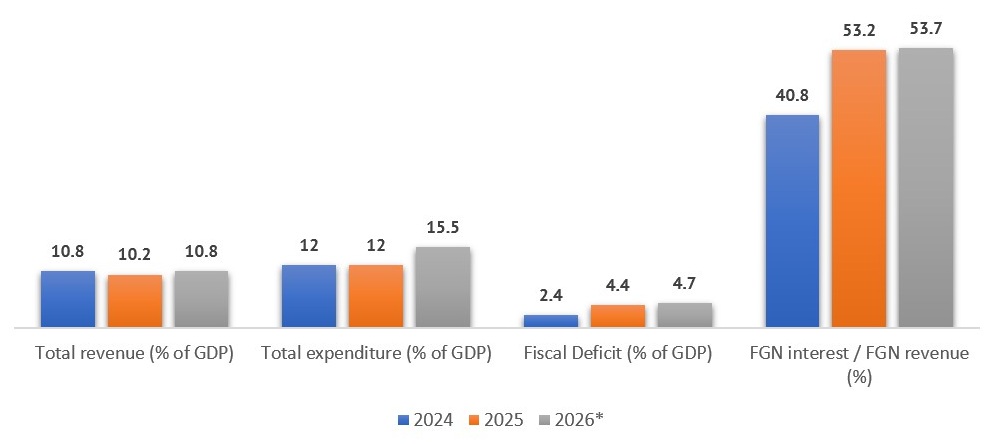

The removal of the fuel subsidy was justified on grounds of market efficiency and social equity. The IMF estimates that eliminating these subsidies generated massive government savings of up to 2.0% of GDP. In standard macroeconomic theory, this fiscal space should allow for significantly higher public investment. In practice, these monumental savings do not appear to have fully accrued to the official 2025 budget. Consolidated general government revenue declined slightly from 10.8% of GDP in 2024 to 10.2% in 2025.

Figure 3: Fiscal Space – Revenue, Expenditure, and Interest burden

Source: IMF, * = forecast

The revenue shortfall was quietly offset by the deliberate under-execution of budgeted capital spending, and more worryingly, by vast expenditures occurring entirely outside the formal budget perimeter. The sheer magnitude of this off-budget activity is captured in an unusually large statistical discrepancy within the national accounts, estimated at 2.7% of GDP for 2025. This suggests a non-trivial share of public expenditure was executed and only retroactively regularised.

Simultaneously, interest payments for the federal government absorbed 53.2% of all federal revenues in 2025. With such an oppressive interest-to-revenue ratio, there is absolutely zero room for discretionary public investment. Within this constrained envelope, social protection spending has not been scaled up, revealing an execution gap that shatters the social compact between the state and its citizens.

The 2027 Political Catalyst and the Rebalancing Act

All of this is unfolding against a sensitive political timetable. With general elections scheduled for early 2027, Nigeria is entering the phase when reform fatigue is most likely to collide with electoral calculus. Historically, the run‑up to elections has been associated with fiscal loosening, off‑cycle wage awards, and policy reversals. The risk now is that the very orthodoxy which has restored macro stability could be diluted or abandoned under pressure from increasingly strained households and mobilised interest groups.

Several disruptive scenarios remain plausible. Although the landmark 2026 tax reforms have now taken effect, structural cost-of-living pressures have triggered aggressive demands from organised labour. The resultant threat of discretionary, unbudgeted public wage concessions threatens to significantly expand the fiscal deficit and complicate near-term debt dynamics.

Consequently, Nigeria requires an urgent transition from aggregate stabilisation to systemic sustainability. Evaluating economic health strictly through the lens of sovereign balance-sheet metrics while internal transmission lines remain broken creates an unsustainable equilibrium. The long-term preservation of Nigeria’s macroeconomic stability depends entirely on the capacity of its institutional frameworks to systematically translate external financial strength into domestic productive capacity, robust physical infrastructure, and genuine household resilience.